The IRS does not get emotional about collections. It just keeps moving — letters, levies, garnishments, one after another — until someone stops it. And when you’re already overwhelmed, the pressure to hire someone fast makes you exactly the kind of person predatory tax relief companies are built to exploit.

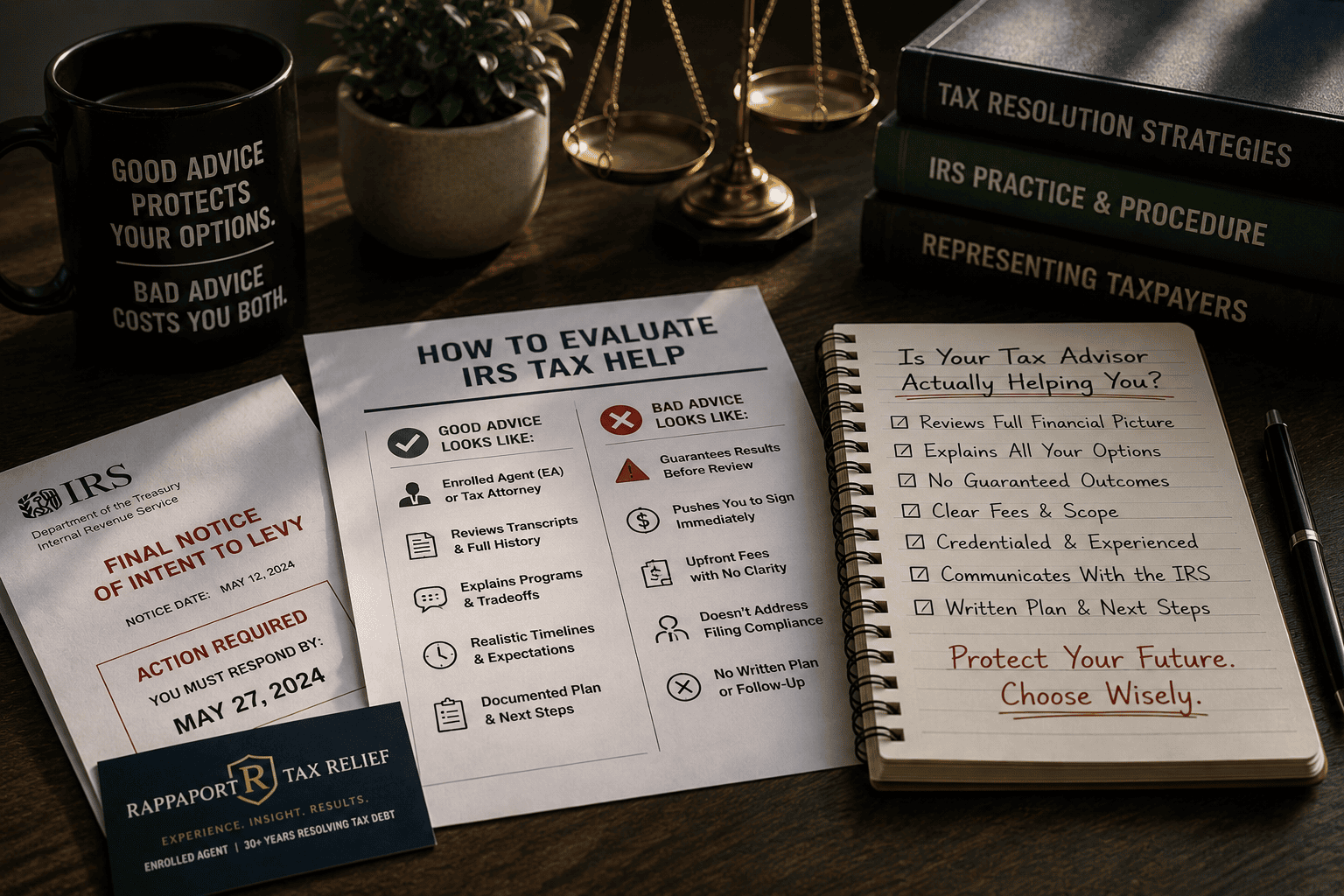

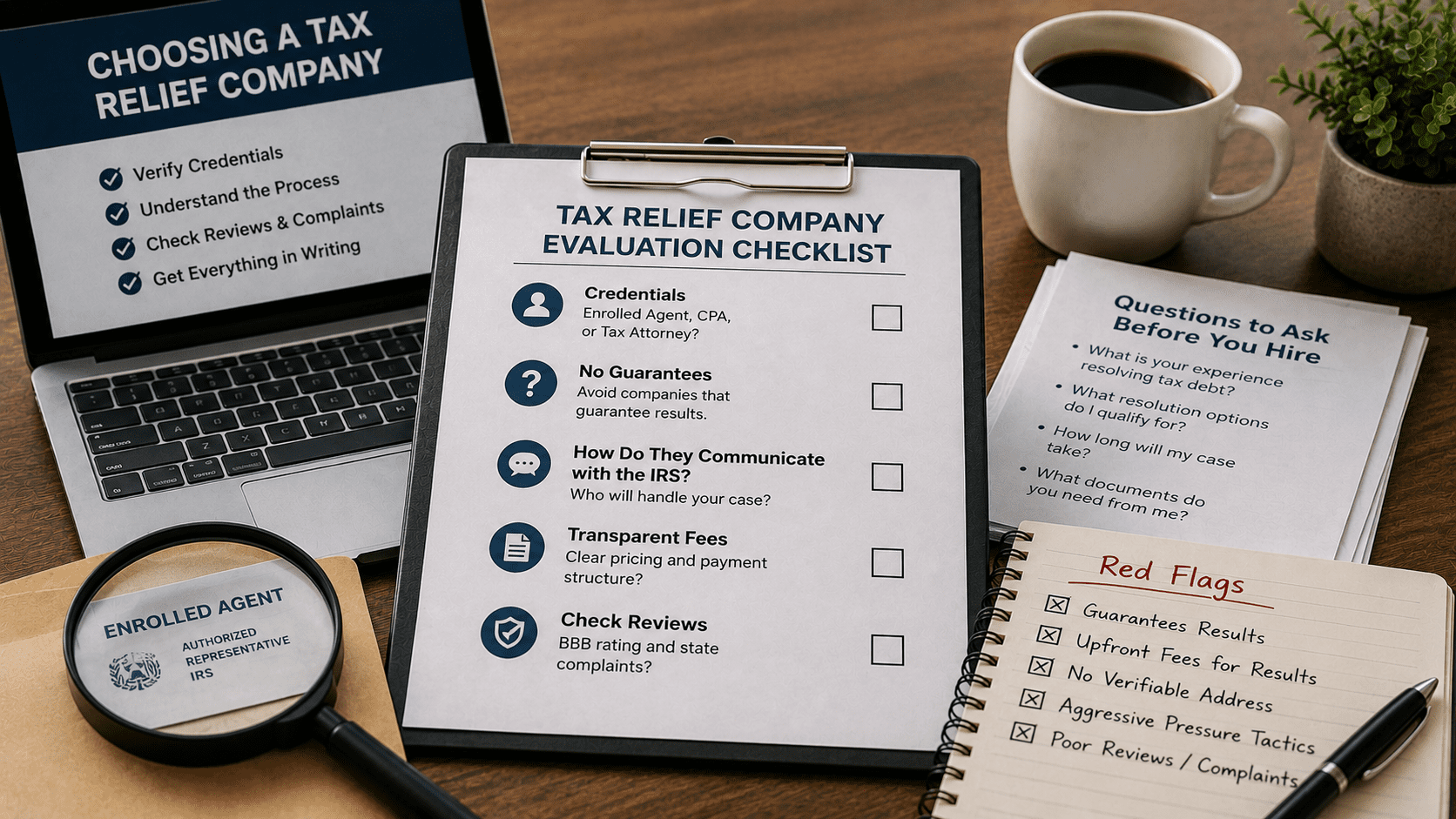

Directly answering the question: To evaluate a tax relief provider without being misled, verify the representative’s credentials (Enrolled Agent, CPA, or tax attorney), confirm they offer a free consultation before charging fees, ask specifically how they communicate with the IRS on your behalf, and check their complaint history with the Better Business Bureau and your state attorney general. Avoid any firm that guarantees a specific outcome before reviewing your case.

Key Takeaways

- Legitimate tax relief providers hold verifiable credentials — Enrolled Agent (EA), CPA, or licensed tax attorney. Ask for the credential number and check it.

- No ethical firm guarantees a specific resolution amount before reviewing your full financial picture.

- The IRS Restructuring and Reform Act of 1998 established taxpayer rights that your representative should be actively using on your behalf — if they can’t name them, that’s a problem.

- Resolution timelines are real: most Installment Agreements take 30–90 days to finalize; Offers in Compromise average 6–12 months per IRS processing guidelines.

- A provider who handles past, present, and future tax issues under one relationship costs less in aggregate than cycling through separate specialists.

Why Do So Many People Hire the Wrong Tax Relief Company?

The tax relief industry is largely unregulated at the marketing level. Anyone can run ads promising to “settle your tax debt for pennies on the dollar.” The credential barrier to advertising tax relief is zero. The barrier to actually practicing before the IRS is significant — but most people don’t know the difference until they’ve already paid a retainer.

This is the root cause: the gap between what a company promises in an ad and what they’re legally authorized to do is invisible to someone who has never navigated IRS collections before. Predatory firms exploit that information asymmetry deliberately.

The mechanism works like this: fear compresses decision-making. When a wage garnishment hits your paycheck or a levy freezes your bank account, the psychological pressure to act immediately overrides the instinct to research carefully. Firms that advertise aggressively know this. They time their outreach — and their urgency language — to catch people at exactly that moment.

The single most expensive mistake in tax resolution isn’t hiring the wrong firm — it’s hiring the wrong firm fast, because panic replaced judgment.

What Credentials Actually Mean — and Which Ones Matter

Enrolled Agent (EA) is the only credential issued directly by the IRS — it grants unlimited practice rights before the IRS at all levels, including audits, collections, and appeals. CPAs and tax attorneys also hold full practice rights. Anyone else — a “tax consultant,” “tax specialist,” or unlicensed preparer — cannot represent you before the IRS in any meaningful capacity.

This distinction is not semantic. If your representative cannot appear before the IRS on your behalf, you are still effectively unrepresented. You’re paying for paperwork help, not advocacy.

The IRS maintains a public directory at irs.gov/tax-professionals where you can verify any EA’s credentials by name. Use it. A legitimate firm will tell you to check.

David Rappaport of Rappaport Tax Relief holds Enrolled Agent status with over 30 years of hands-on IRS negotiation experience — the kind of practitioner-level depth that comes from working actual cases, not just knowing the code.

The Practitioner’s Evaluation Framework: The CLEAR Test

The CLEAR Test is a five-point evaluation framework for assessing any tax relief provider before signing anything or paying a retainer.

Use this when you’re comparing providers or feeling pressured to decide quickly. Skip it only if you’ve already verified credentials independently and have a referral from someone whose situation matched yours.

| Criterion | What to Ask | Red Flag |

| C — Credentials | “What is your EA or CPA license number?” | Vague titles, no verifiable number |

| L — Limitations Disclosed | “What outcomes can you NOT guarantee?” | Any firm that won’t name limitations |

| E — Explicit Process | “Walk me through exactly what happens after I hire you.” | Generic answers, no IRS-specific steps |

| A — Access to Principal | “Who personally handles my case?” | “A team” with no named practitioner |

| R — Resolution Range | “What’s a realistic range of outcomes for my situation?” | Specific dollar promises before case review |

A firm that passes all five without hesitation is worth a serious conversation. A firm that stumbles on two or more is telling you something important.

What Does “Concierge” Tax Resolution Actually Mean in Practice?

Most national tax relief firms operate on volume. Your case is assigned to a case manager — not a credentialed practitioner — who follows a script and escalates when things get complicated. You may never speak to the person who actually knows tax law.

Concierge tax resolution is the opposite model: one credentialed practitioner manages your case from intake through resolution, knows your file, and is reachable when something changes.

Why this matters mechanically: IRS collection cases are not static. A revenue officer can escalate, a levy can be issued between scheduled calls, a Collection Due Process hearing deadline can pass. When your case is handled by someone who knows it deeply, those developments get caught and responded to. When it’s handled by a rotating case manager working from notes, they don’t.

Rappaport Tax Relief operates on this model specifically. David Rappaport personally handles client cases — not a junior associate, not a call center. That’s not a marketing line. It’s a structural difference in how the work gets done.

Knowing your case file is not a luxury in tax resolution — it’s the difference between catching a deadline and missing it permanently.

What Realistic Outcomes Actually Look Like (With Numbers)

Here’s what practitioners commonly observe across resolution types — not guarantees, but honest ranges based on IRS program parameters.

Installment Agreement: A self-employed contractor with $34,000 in back taxes and no prior defaults can typically establish a streamlined installment agreement within 30–60 days. Monthly payments are based on ability to pay, not the full balance divided arbitrarily.

Offer in Compromise (OIC): The IRS accepted roughly 13,000–15,000 OICs annually in recent reporting years (IRS Data Book). Acceptance is based on Reasonable Collection Potential — a specific IRS formula weighing assets, income, and allowable expenses. A business owner three years into penalty accrual, with $67,000 in assessed liability but documented income below IRS Collection Financial Standards, resolved to $11,200 over 11 months through an accepted OIC. That outcome required a complete financial disclosure, accurate documentation, and a practitioner who knew how to present the case — not just file the form.

Currently Not Collectible (CNC) Status: For clients with income at or near IRS allowable expense thresholds, CNC status pauses collection activity entirely. It doesn’t eliminate the debt, but it stops the bleeding while circumstances change.

Rappaport Tax Relief works across all three resolution tracks — and the right path depends entirely on your specific financial picture, not on which program sounds most appealing.

Who This Approach Is NOT Right For

Honest assessment matters here.

Tax resolution services are not the right fit if your total IRS liability is under $5,000 and you have the income to pay it — in that case, a direct IRS payment plan costs nothing to set up and requires no representation.

If your situation involves criminal tax fraud allegations, you need a tax attorney with criminal defense experience, not an Enrolled Agent. EA authority covers civil IRS matters; criminal exposure is a different legal domain entirely.

And if you’re looking for someone to make the problem disappear without your participation — providing financial documents, disclosing income accurately, responding to information requests — no legitimate firm can help you. Resolution requires cooperation. Any firm that promises otherwise is not being straight with you.

Frequently Asked Questions

How do I know if a tax relief company is legitimate before I pay them anything? Ask for the practitioner’s Enrolled Agent, CPA, or bar license number and verify it independently through the IRS directory or your state licensing board. Legitimate firms welcome this. Also check the Better Business Bureau and your state attorney general’s complaint database — volume complaints about upfront fees with no follow-through are a consistent pattern with bad actors.

What’s the difference between an Enrolled Agent and a tax attorney for IRS problems? Both hold unlimited practice rights before the IRS, meaning either can represent you in audits, collections, and appeals. Tax attorneys are better suited when there’s potential criminal exposure or complex litigation. Enrolled Agents typically specialize more deeply in IRS procedure and resolution programs — for most collection cases, an experienced EA is exactly the right credential.

Can a tax relief company actually get my wage garnishment stopped quickly? Yes, but “quickly” depends on your situation. Once a practitioner files a power of attorney and contacts the IRS, a garnishment release can sometimes be negotiated within days if you qualify for a resolution program. The IRS does not release garnishments as a courtesy — there needs to be an active resolution in place or a pending appeal. Rappaport Tax Relief handles garnishment releases directly as part of the resolution process.

What happens if I’ve had unfiled tax returns for several years? Unfiled returns don’t disappear — the IRS can file a Substitute for Return (SFR) on your behalf, which almost always results in a higher liability than if you’d filed yourself. Getting into compliance by filing past returns is usually the first step in any resolution process. Practitioners commonly observe that clients who file voluntarily receive more favorable treatment than those whose returns were filed by the IRS.

Is an Offer in Compromise realistic for someone with a modest income? It can be. The OIC program is specifically designed for taxpayers whose Reasonable Collection Potential — what the IRS calculates they can actually collect — is less than the full liability. Modest income can actually support an OIC application if allowable expenses are documented correctly. The form is not the hard part; the financial presentation is.

How long does it take to resolve IRS tax debt completely? It depends on the resolution path. Installment Agreements: 30–90 days to establish. Offers in Compromise: 6–12 months for IRS processing after submission. Currently Not Collectible status: can be established relatively quickly but requires annual review. Complex cases with multiple years of unfiled returns can take longer — but every month without representation is a month of continued penalty and interest accrual.

What should I bring to a free consultation with a tax relief firm? Bring any IRS notices you’ve received (the notice number in the top right corner tells a practitioner exactly what stage of collection you’re in), your most recent tax returns if you have them, and a general sense of your monthly income and expenses. You don’t need everything organized — a good practitioner will tell you exactly what they need after hearing your situation.

The One Thing That Changes How You See This Entire Category

Most people treat tax relief as a transaction: pay someone to negotiate a number down. That framing leads to hiring whoever quotes the lowest fee or promises the biggest reduction.

The more accurate frame: tax resolution is access management. The IRS has a defined set of programs, each with specific eligibility criteria and procedural requirements. A skilled practitioner’s job is to get you into the right program, present your case correctly, and keep the process moving. The outcome is a function of your financial reality and the quality of the presentation — not the boldness of the promise.

That’s what 30 years of hands-on IRS negotiation actually buys you. Not magic. Precision.

If you’re at the point where you’ve read this far, you’re not looking for a quick fix. You’re looking for someone who will actually handle this — past baggage, present crisis, and a path forward that doesn’t leave you back here in three years.

That’s exactly what Rappaport Tax Relief does. Schedule your free consultation and talk directly with David Rappaport about where you stand and what’s actually possible for your situation.

References

IRS.gov — IRS Data Book (annual publication covering OIC acceptance rates, collection statistics, and taxpayer compliance data)

IRS.gov — Taxpayer Rights under the IRS Restructuring and Reform Act of 1998

IRS.gov — Offer in Compromise program eligibility and Reasonable Collection Potential calculation methodology

IRS.gov — Tax Professional Directory (credential verification for Enrolled Agents)

Better Business Bureau (bbb.org) — Consumer complaint database for tax relief companies