The IRS collected more than $98 billion in enforcement revenue in a recent fiscal year, and that number keeps climbing. If you’re carrying tax debt right now, you’re not dealing with a slow-moving bureaucracy. You’re dealing with a machine that doesn’t pause, doesn’t negotiate on its own, and doesn’t care that you didn’t understand what you owed.

Tax relief in 2026 looks different than it did five years ago. Some resolution paths have opened up. Others have quietly closed. Knowing which is which could be the difference between a manageable payment plan and a bank levy that empties your account on a Tuesday morning.

Direct Answer

Tax relief still works in 2026. But the strategies that produce results have shifted. Offer in Compromise acceptance remains selective, installment agreements are more accessible than most people realize, and IRS enforcement has accelerated after years of staffing rebuilds. The taxpayers who get the best outcomes are those who act before the IRS escalates, not after.

Key Takeaways

- Offer in Compromise is not a universal fix. It works for a specific financial profile, and most people who apply without professional help get rejected

- Installment agreements are currently one of the most reliable resolution tools for moderate debt, but the terms you negotiate upfront determine how painful the next few years feel

- IRS enforcement timelines have shortened. Wage garnishments and bank levies are arriving faster than they were two years ago

- Penalty abatement is one of the most underused relief options available, and it requires no special financial hardship to qualify

- Waiting to act is not a neutral choice. Every month of inaction adds interest, compounding penalties, and narrows the resolution options still available to you

What Has Actually Changed About Tax Relief in 2026?

The IRS isn’t the same agency it was in 2021. After years of understaffing and pandemic-era collection pauses, enforcement capacity has been rebuilt. The LT11 letters are going out faster. The CP14 notices are following up sooner. The gap between “first notice” and “levy action” has compressed.

What this means practically: the window to resolve a tax problem before it becomes a collection crisis is shorter now than it’s been in years.

For taxpayers in Connecticut and the broader New England area, this shift is real and measurable. Practitioners who work IRS cases daily are seeing faster escalation timelines and less tolerance for informal delays.

The core resolution tools haven’t changed. Offer in Compromise, installment agreements, Currently Not Collectible status, penalty abatement. But the conditions under which each one works have shifted. Here’s what’s actually working now.

What’s Working: The Resolution Tools With Real Traction Right Now

- Streamlined Installment Agreements

For taxpayers who owe under $50,000 and have filed all required returns, streamlined installment agreements remain one of the most accessible and reliable paths to resolution. The IRS approves these without requiring a full financial disclosure, which speeds up the process considerably.

The catch most people miss: the monthly payment amount matters enormously. If you accept the IRS’s initial payment proposal without negotiating, you may lock yourself into terms that strain your budget for years. A qualified representative can push back on that number using allowable expense standards. And often get it reduced.

If you’re wondering how installment agreements for federal income taxes actually work in practice, the mechanics matter as much as the eligibility.

- Penalty Abatement. Especially First-Time Abatement

First-Time Abatement (FTA) is the IRS’s own program for removing penalties from taxpayers who have a clean compliance history. If you’ve filed and paid on time for the three years before the year in question, you may qualify to have failure-to-file or failure-to-pay penalties removed entirely.

Most people don’t know this exists. The IRS doesn’t advertise it. And it doesn’t require financial hardship. Just a clean prior record.

This is one of the most underused tools in tax resolution, and it can eliminate thousands of dollars in penalties without the complexity of an Offer in Compromise.

- Currently Not Collectible (CNC) Status

If your income genuinely doesn’t cover basic living expenses after the IRS’s own allowable expense calculations, you may qualify for CNC status. The IRS temporarily suspends collection activity, no levies, no garnishments, while your account sits in this status.

It’s not permanent, and interest continues to accrue. But for someone in a genuine financial crisis, it buys time to stabilize without the threat of enforcement action overhead.

- Offer in Compromise. For the Right Profile

Offer in Compromise (OIC) is the most talked-about tax relief tool and the most misunderstood. An OIC is a settlement where the IRS agrees to accept less than the full amount owed. But only when it calculates that you genuinely can’t pay the full balance over the remaining collection statute.

The IRS’s acceptance rate for OICs is not high. The taxpayers who succeed are those whose Reasonable Collection Potential, the IRS’s formula for what you can realistically pay, actually comes in below what they owe. If you want to understand whether you might qualify, the OIC eligibility criteria in Connecticut lay out the key factors clearly.

What Has Stopped Working (Or Never Worked the Way People Think)

Ignoring IRS notices and hoping the problem resolves itself.

It won’t. The IRS doesn’t forget. It doesn’t get tired. And every month you wait, the penalty and interest balance grows. Failure-to-pay penalties accrue at 0.5% per month on the unpaid balance. That’s not catastrophic on its own. But compounded over two or three years, it adds up to a debt that’s meaningfully larger than what you originally owed.

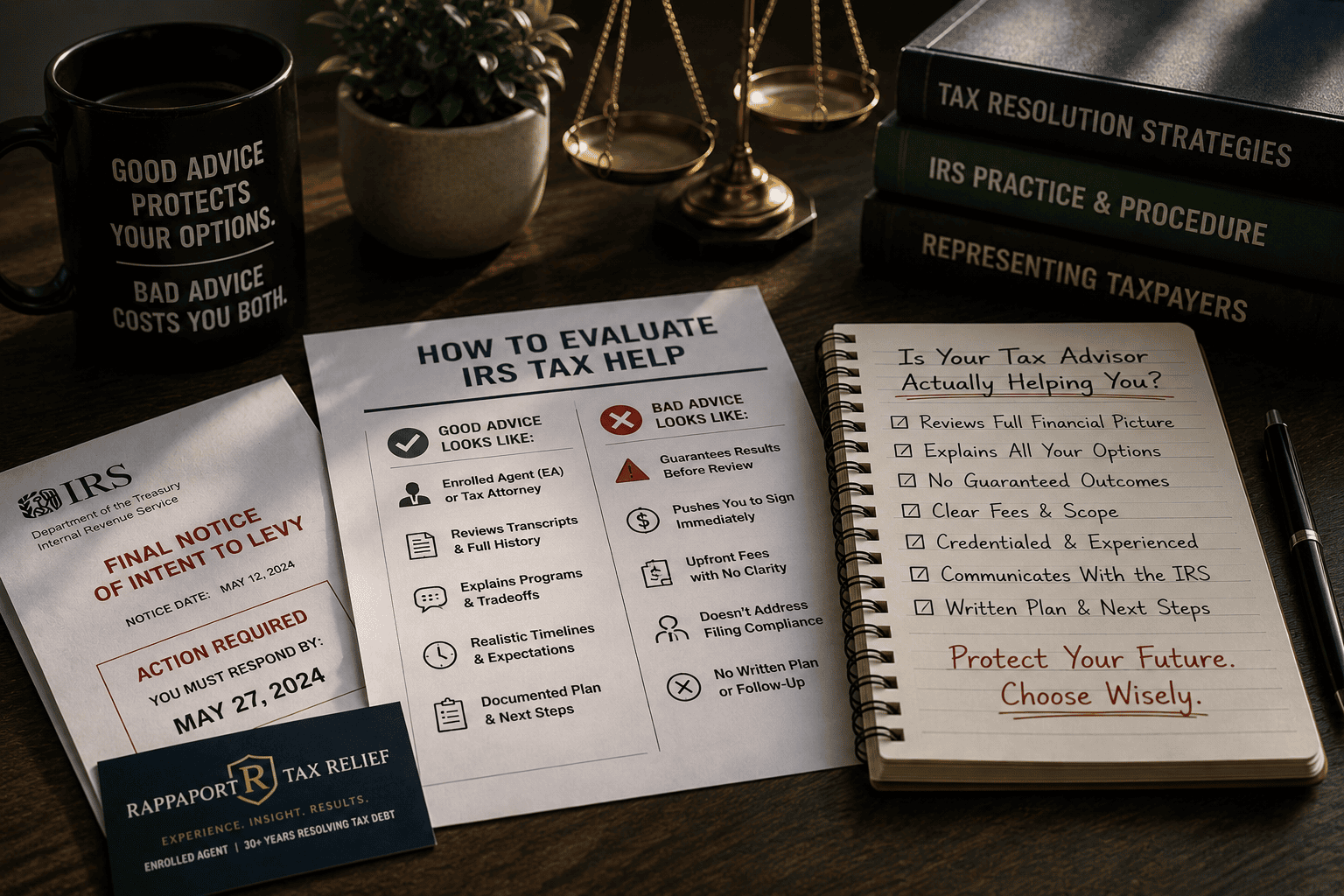

DIY Offer in Compromise submissions.

The IRS’s OIC pre-qualifier tool gives people false confidence. Calculating Reasonable Collection Potential correctly requires knowing which expense allowances apply to your situation, how to value assets the IRS will scrutinize, and how to present your financial picture in a way that supports your case. A rejected OIC doesn’t just waste time. It can reset the collection clock and signal to the IRS that you have assets worth pursuing.

Hiring a national tax relief firm based on a late-night TV ad.

This is where real damage happens. Predatory firms exploit the information gap between what taxpayers know and what the IRS process actually requires. They collect large upfront fees, make promises about settlements they can’t guarantee, and then disappear or produce nothing. The FTC has taken action against multiple national firms for exactly this pattern.

The most confident pitch is often the least trustworthy signal.

The Resolution Decision Matrix: Which Path Fits Your Situation?

Use this framework, call it the Tax Debt Triage Model, to identify which resolution path matches your actual circumstances. It’s not a substitute for professional analysis, but it helps you understand the landscape before your first conversation.

| Your Situation | Most Likely Path | What to Watch For |

| Owe under $50K, all returns filed | Streamlined Installment Agreement | Negotiate payment amount. Don’t accept the IRS’s first proposal |

| Clean prior compliance history | First-Time Penalty Abatement | Apply before paying. Approval removes the penalty, not just defers it |

| Income below IRS expense allowances | Currently Not Collectible status | Temporary. Reassessed annually; interest still accrues |

| Low income, few assets, large debt | Offer in Compromise | Requires full financial disclosure; rejection is common without professional help |

| Unfiled returns + active enforcement | File first, then resolve | Can’t negotiate while non-compliant. Filing is the prerequisite |

| Wage garnishment already active | Immediate representation needed | Garnishments can be released, but timing and documentation matter |

Why Going It Alone Costs More Than It Saves

Here’s the contrarian truth most people don’t want to hear: the cost of professional representation is almost always smaller than the cost of a mistake made without it.

Consider a typical case: a self-employed contractor in Connecticut owes $28,000 in back taxes across three years. He files his own OIC, underestimates his Reasonable Collection Potential by failing to account for a vehicle the IRS values differently than he does, and gets rejected. The IRS now has a fuller picture of his finances and begins levy proceedings. What could have been a negotiated installment agreement at a manageable monthly payment becomes a bank levy and a much harder negotiation from a weaker position.

The mechanism here isn’t complexity. It’s information asymmetry. The IRS knows its own formulas. Most taxpayers don’t. A representative who works these cases every day closes that gap.

Rappaport Tax Relief, based in Westport, Connecticut, operates on exactly this principle. David Rappaport has spent 30+ years working IRS cases directly. Not delegating them to junior staff, not running a volume-based call center. If you’re dealing with a wage garnishment that’s already started, that kind of direct attention isn’t a luxury. It’s what determines whether the garnishment gets released or drags on for months.

Who Gets the Best Outcomes From Tax Relief. And Who Doesn’t

Tax relief works best when you act before the IRS escalates to enforced collection. The further along the enforcement chain you are, from notice to lien to levy to garnishment, the fewer options remain and the harder each one is to execute.

It works least well when:

- Returns are still unfiled (you can’t negotiate while non-compliant. Filing is the prerequisite for everything else)

- The taxpayer has significant assets the IRS can reach (OIC becomes nearly impossible)

- The debt is primarily from trust fund taxes (payroll taxes carry personal liability that doesn’t disappear in most resolution paths)

Rappaport Tax Relief is direct about this. Not every situation ends in a dramatic settlement. Some cases resolve through structured payment plans. Some through penalty removal. Some through a combination. What matters is getting the right resolution for your actual situation. Not the one that sounds best in a sales pitch.

Waiting feels safe. It’s actually the most expensive move you can make.

Frequently Asked Questions

How do I know if I actually qualify for an Offer in Compromise?

The IRS uses a formula called Reasonable Collection Potential to decide whether to accept an OIC. It looks at your income, expenses, and asset equity. If what you can realistically pay over the remaining collection period is less than what you owe, you may qualify. But the calculation is specific and unforgiving. A professional can run the numbers before you submit anything.

What happens if I just ignore IRS notices and don’t respond?

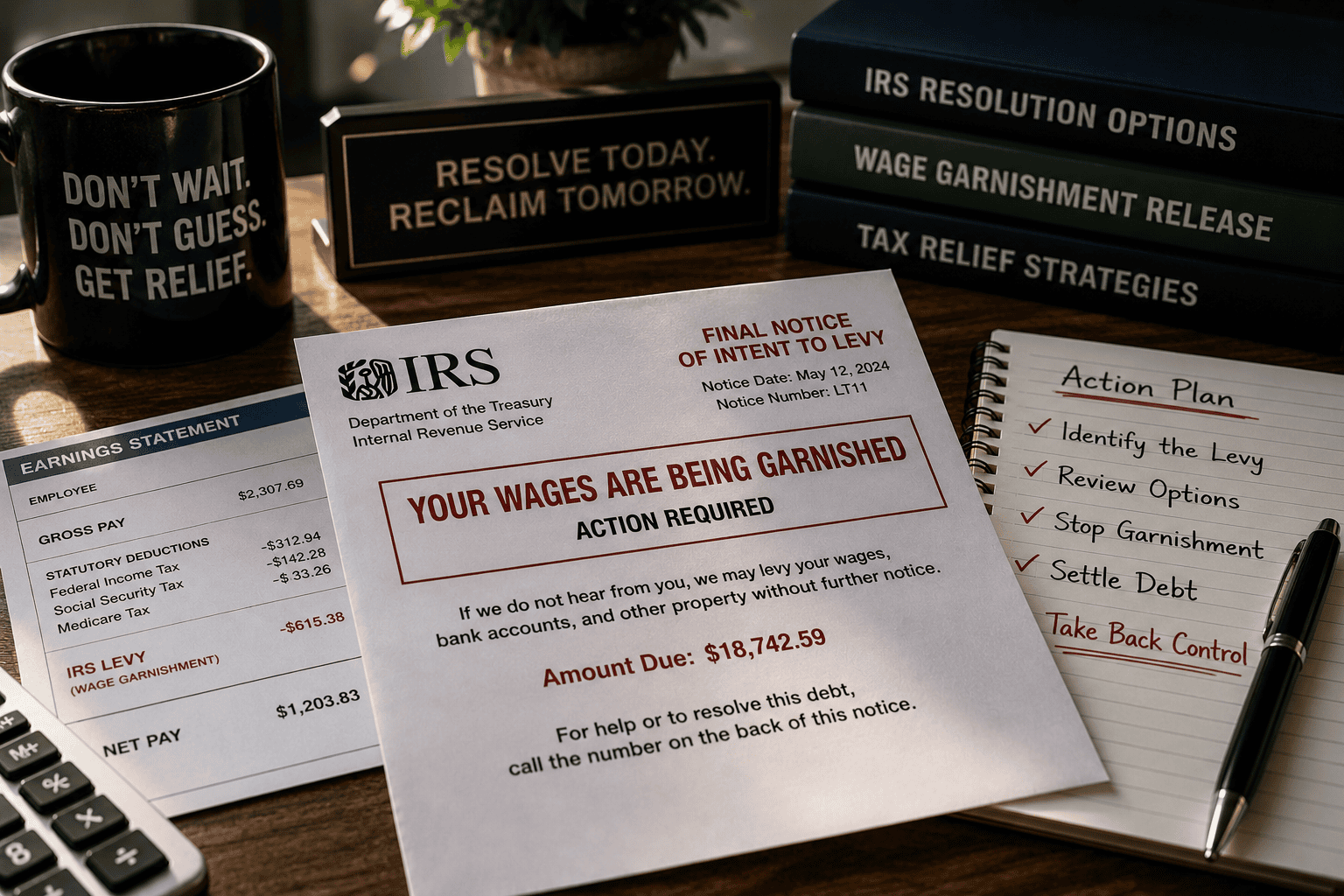

The IRS escalates automatically. A CP14 becomes an LT11, which becomes a Notice of Intent to Levy, which becomes an actual levy on your bank account or wages. There’s no point in the sequence where ignoring the problem makes it smaller. The collection statute is ten years. The IRS has time, and it uses it.

Can the IRS really garnish my wages without warning?

Not entirely without warning. The IRS is required to send a Final Notice of Intent to Levy before taking wage action. But that notice can arrive and go unnoticed, especially if you’ve moved or aren’t opening mail. By the time you feel the garnishment, the IRS has already completed the required steps. Acting on the first notice is always better than responding to the last one.

Is it too late to get help if a levy has already started?

No. Levies can be released. But it requires immediate action and documentation. The IRS will release a levy if you enter into an approved resolution agreement, demonstrate financial hardship, or show the levy is creating an economic hardship that prevents you from meeting basic living expenses. Rappaport Tax Relief handles IRS levy situations directly and can move quickly when enforcement is already active.

What’s the difference between a tax lien and a tax levy?

A lien is a legal claim against your property. It affects your credit and your ability to sell assets, but it doesn’t take anything immediately. A levy is the actual seizure: your bank account drained, your wages redirected to the IRS. Liens come first; levies follow if the lien doesn’t produce payment. Both are serious, but levies require faster response.

How long does tax resolution actually take?

It depends on the path. A streamlined installment agreement can be established in a few weeks. An Offer in Compromise typically takes six to twelve months from submission to decision. Currently Not Collectible status can be requested relatively quickly once financial documentation is assembled. There are no shortcuts, but there are faster and slower paths depending on your situation.

Do I need a tax attorney, or is an Enrolled Agent enough?

For most IRS collection and resolution cases. Installment agreements, OICs, penalty abatement, levy releases. An Enrolled Agent has full authority to represent you before the IRS. Tax attorneys add value when litigation is involved or when there are complex legal questions about liability. David Rappaport’s 30+ years as an Enrolled Agent covers the full range of resolution cases that most individuals and small businesses face.

You’ve Read This Far. Here’s the Next Step

If any section of this article described your situation, you already know what the next move is. Not because it’s the comfortable choice. But because you’ve just seen what happens when people wait.

Rappaport Tax Relief offers a free consultation. Not a sales call. A real conversation about your specific situation, what options are realistically available, and what happens if you do nothing. Call or reach out directly. David Rappaport handles these conversations personally.

About the Author

Rappaport Tax Relief is a tax resolution firm based in Westport, Connecticut, specializing in IRS debt negotiation, penalty abatement, installment agreements, and Offer in Compromise representation. Led by Enrolled Agent David Rappaport with more than 30 years of hands-on experience, they serve individuals, self-employed professionals, and small business owners across Connecticut and New England who are dealing with IRS collection activity and need direct, personal representation. Not a call center.

References

IRS via Experian. Standard deduction amounts for 2025 tax year