The IRS does not get emotional about collections. It just keeps moving — adding penalties, compounding interest, escalating to levies and garnishments — while most people are still deciding whether to open the envelope. That gap between the IRS’s momentum and a taxpayer’s paralysis is where most tax situations go from bad to genuinely damaging.

Direct Answer

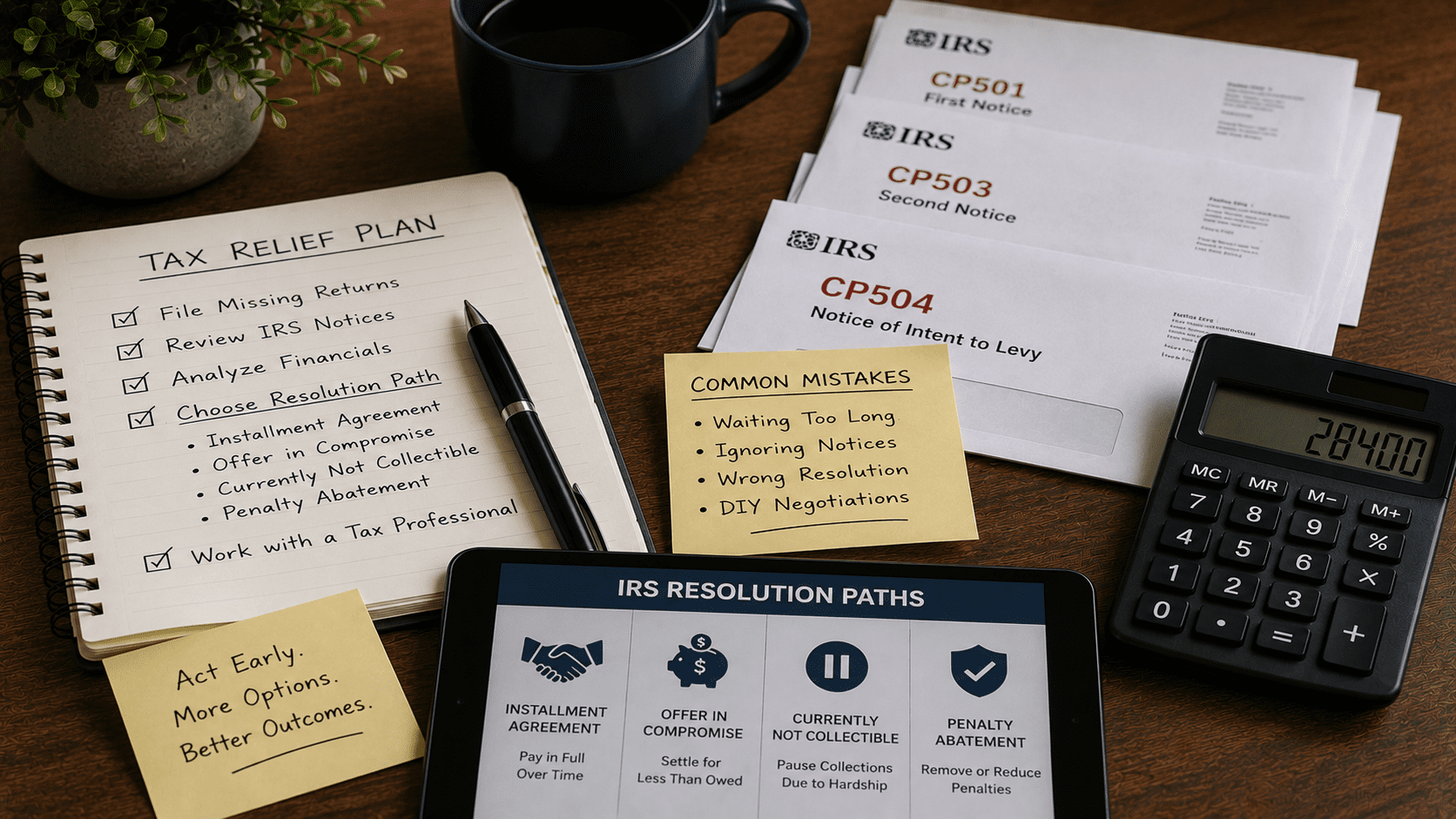

The most common tax relief mistakes people make are waiting too long to act, attempting to negotiate with the IRS without representation, ignoring notices until enforcement begins, and choosing resolution paths that don’t match their actual financial situation. These mistakes persist not from carelessness but because the IRS system is designed around compliance, not guidance — leaving taxpayers to navigate it alone.

Key Takeaways

- Ignoring IRS notices doesn’t pause the process — it accelerates enforcement timelines and reduces your negotiating options

- Filing late returns, even without payment, stops the penalty clock and reopens resolution pathways that disappear without filed returns

- An Offer in Compromise is not available to everyone — qualifying requires specific financial conditions, and applying incorrectly wastes time and fees

- Installment agreements negotiated without professional help often set monthly payments higher than necessary, creating a new financial crisis

- Enrolled Agents have federally recognized authority to represent taxpayers before the IRS — a distinction that matters when negotiating collection holds

Why Do People Wait So Long to Deal with IRS Debt?

Avoidance is not laziness. It is a predictable response to a system that feels punishing to engage with.

When people receive IRS notices, the instinct is to set them aside until they feel “ready” — financially, emotionally, or practically. The problem is that the IRS operates on fixed statutory timelines. The Collection Statute Expiration Date (CSED) — the 10-year window the IRS has to collect assessed tax debt — does not pause because a taxpayer is overwhelmed. More critically, certain resolution options narrow or close entirely as enforcement escalates.

Waiting does not preserve your options. It eliminates them.

Consider a business owner three years into penalty accrual on a significant payroll tax debt. The balance had grown substantially before they sought help — not because they ignored it intentionally, but because they kept expecting cash flow to recover enough to simply pay it. When they finally engaged Rappaport Tax Relief, the resolution pathway was still available, but the negotiating position had weakened considerably. Had they acted earlier, the balance and the timeline both would have been smaller.

The mechanism here matters: penalties under IRS Code Section 6651 compound monthly. Every month of inaction is not neutral — it is actively expensive. Understanding when to act and when to wait on tax relief can mean the difference between a manageable resolution and a far more costly one.

Is Trying to Handle IRS Debt Yourself Actually a Bad Idea?

Yes. Not because taxpayers are incapable, but because the IRS negotiation process rewards procedural knowledge that takes years to develop.

The IRS’s Automated Collection System (ACS) is staffed by agents working from scripts and authority limits. A taxpayer calling in without representation is negotiating blind — they don’t know what the agent can actually approve, what financial information to disclose or withhold, or which collection alternative fits their situation. Practitioners report that self-represented taxpayers routinely agree to installment payment amounts that exceed what a professional would have negotiated, because they don’t know that Collection Financial Standards — the IRS’s own benchmark for allowable living expenses — can be used to lower the required monthly payment.

> The IRS is not your adversary, but it is not your advisor either. It will accept whatever you agree to, even if a better option existed.

This is worth sitting with: the IRS does not tell you about resolution options you don’t ask for. Offer in Compromise, Currently Not Collectible status, Penalty Abatement — these are not offered proactively. They require a taxpayer or their representative to initiate and document the request correctly.

Rappaport Tax Relief handles this negotiation on behalf of clients, using more than 30 years of direct IRS experience to identify which pathway fits the actual financial picture — not the one that sounds best in a brochure.

What Is the “Wrong Resolution” Mistake and Why Does It Cost So Much?

Choosing the wrong resolution path is the most expensive mistake most people have never heard of.

The three primary IRS resolution options — Installment Agreement, Offer in Compromise (OIC), and Currently Not Collectible (CNC) status — each have distinct eligibility criteria, cost structures, and long-term implications.

The Resolution Fit Framework is a simple diagnostic tool for understanding which path applies:

| Resolution Path | Use When | Not When |

| Installment Agreement | You can pay the full balance over time | Monthly payment would create financial hardship |

| Offer in Compromise | Your Reasonable Collection Potential (RCP) is less than what you owe | You have assets or income that disqualify you |

| Currently Not Collectible | You have no disposable income after IRS-allowed expenses | You have irregular income that could qualify you for OIC |

| Penalty Abatement | You have a clean compliance history and a reasonable cause | You have prior penalty abatement in the last 3 years |

Use this framework as a starting diagnostic — not a final determination. Eligibility has layers.

The OIC mistake is particularly common. National tax relief advertising has made “settle your debt for pennies on the dollar” a cultural shorthand — but the IRS accepts only a fraction of OIC applications, and applying without meeting the financial threshold wastes months and fees while enforcement continues.

> Choosing the wrong IRS resolution path doesn’t just fail — it delays the right path and gives the IRS more time to collect.

Why Do Unfiled Returns Create More Damage Than Unpaid Taxes?

This is the observation that surprises most people: owing money to the IRS is a problem; not filing is a crisis.

Unfiled returns trigger the IRS’s Substitute for Return (SFR) process — the IRS files a return on your behalf using only the income information it has, with no deductions, no credits, and no context. The resulting tax assessment is almost always inflated, and it starts the penalty and interest clock immediately.

More critically, an SFR assessment locks you out of certain resolution options until the correct return is filed. You cannot negotiate an Offer in Compromise on an SFR balance. You cannot establish a formal installment agreement in good standing. The IRS requires full compliance — all returns filed — before most resolution pathways open.

Filing, even without the ability to pay, is always the right first move. It stops the SFR process, establishes the accurate balance, and reopens negotiating options. This feels counterintuitive: filing a return that shows you owe money feels like making the problem worse. It actually makes it solvable.

Rappaport Tax Relief regularly helps clients file multiple years of back returns as the first step in a resolution plan — because without that foundation, nothing else can move forward.

Does Hiring a National Tax Relief Company Actually Help?

Sometimes. But the tradeoffs are real and worth understanding.

National tax relief firms operate at volume. They use intake teams, case managers, and rotating representatives — meaning the person who assessed your situation is rarely the person negotiating with the IRS on your behalf. Clients of large national firms often wait months before substantive IRS contact is made, while penalties continue to accrue. Knowing how to tell if a tax relief company is actually going to help you before signing anything can save significant time and money.

The structural difference with a concierge approach — like the one Rappaport Tax Relief provides — is continuity. David Rappaport, an Enrolled Agent with more than 30 years of IRS negotiation experience, handles client cases personally from the firm’s Westport, Connecticut office. The person who knows your financial situation is the person speaking to the IRS. That continuity is not a comfort feature. It is a negotiating advantage, because the IRS responds to representatives who can answer questions in real time without putting the call on hold to check a file.

| Factor | National Firm | Concierge EA (Rappaport) |

| Case handler continuity | Often rotates | Single practitioner |

| IRS contact timeline | Can be delayed | Initiated promptly |

| Personalization | Standardized intake | Individual financial analysis |

| Geographic familiarity | Generic | Connecticut and surrounding area context |

| Fee structure | Often upfront, large retainer | Transparent, case-specific |

The One Insight Worth Bookmarking

The IRS’s collection system is not designed to find the resolution that helps you most — it is designed to collect as much as possible, as quickly as possible. Getting the outcome you deserve requires someone who knows how to ask for it.

Who Is Tax Relief Representation NOT Right For?

Honest answer: not everyone needs full representation.

If you have a single year of unfiled returns, a straightforward income history, and the ability to pay the balance in full within 120 days, a self-service IRS payment arrangement may be sufficient. The IRS’s Online Payment Agreement tool handles simple cases without professional involvement.

Rappaport Tax Relief is built for situations with more complexity: multiple years of debt, active enforcement like wage garnishments or bank levies, business payroll tax issues, or cases where the balance has grown significantly through penalties. If your situation is simple and contained, say so during a free consultation — an honest practitioner will tell you when you don’t need them.

What this service does not do: it does not provide criminal defense for tax fraud or evasion. Those situations require a tax attorney with criminal law experience. Enrolled Agent authority covers civil IRS matters — audits, collections, appeals, and resolution — not criminal proceedings. For those who want to understand how Rappaport Tax Relief actually works from end to end, that process is laid out in detail for prospective clients before any engagement begins.

Frequently Asked Questions

How long does it actually take to resolve IRS debt? Resolution timelines vary by case complexity, but most straightforward installment agreements are established within 60 to 90 days of engagement. Offer in Compromise cases typically take 6 to 12 months from submission to IRS decision, sometimes longer if the IRS requests additional documentation. Cases involving unfiled returns add time at the front end, because returns must be filed before resolution negotiations can formally begin.

Will the IRS really negotiate with me, or is that just marketing? The IRS does negotiate — but only within specific programs it administers, and only when the taxpayer or their representative initiates the request with proper documentation. The IRS does not proactively offer you the best available option. It accepts what you agree to. Having a representative who knows what to ask for, and how to document it, is what makes negotiation meaningful rather than performative.

What happens if I just ignore IRS notices and hope they go away? They don’t go away. The IRS follows a structured notice sequence — CP14, CP501, CP503, CP504, and then enforcement action — and each stage escalates collection authority. Ignoring notices does not pause this sequence; it advances it. Once the IRS issues a Final Notice of Intent to Levy, they can garnish wages, seize bank accounts, or place liens on property. Acting before that final notice is issued preserves significantly more options.

Can I get my wage garnishment stopped quickly? Yes, in most cases a wage garnishment can be released relatively quickly once a resolution pathway is established. The IRS will typically release a levy when a taxpayer enters into an installment agreement or demonstrates financial hardship. The process requires direct IRS contact, proper documentation, and in some cases same-day or next-day action. Rappaport Tax Relief has helped clients stop garnishments before the next payroll cycle.

Is an Offer in Compromise actually realistic for someone with a modest income? It can be, and modest income is actually one factor that can support OIC eligibility. The IRS calculates your Reasonable Collection Potential (RCP) — essentially what they believe they can actually collect from you — and if that number is less than the total balance owed, an OIC may be viable. The mistake is assuming you qualify without a proper financial analysis, or assuming you don’t qualify without one. A professional assessment is the only way to know.

What’s the difference between an Enrolled Agent and a CPA or tax attorney for IRS issues? An Enrolled Agent (EA) is a federally licensed tax practitioner with unlimited rights to represent taxpayers before the IRS — including audits, collections, and appeals. CPAs and attorneys can also represent taxpayers, but their core training is in accounting and law respectively. EAs specialize specifically in taxation and IRS procedure. For IRS collection and resolution work, an experienced EA often has more direct, specialized IRS negotiation experience than a general CPA or attorney.

What should I bring to a first consultation with a tax relief professional? Bring any IRS notices you’ve received, your most recent tax returns (or note how many years are unfiled), a general sense of your income and major assets, and any correspondence about garnishments or levies. You don’t need everything organized perfectly — the consultation is designed to assess your situation, not audit you. The goal of the first conversation is to understand what you’re dealing with and identify the fastest path to stopping enforcement.

You Don’t Have to Keep Carrying This

If you’ve read this far, you’re not someone who doesn’t care about resolving this. You’re someone who hasn’t known where to start — or who started in the wrong place and got burned.

Rappaport Tax Relief offers free consultations because the first step shouldn’t cost you anything. Call or reach out at rappaporttaxrelief.com, tell David what you’re dealing with, and get a straight answer about what your options actually are. Not a sales pitch. Not a generic plan. A real conversation about your specific situation — from someone who has resolved cases like yours for more than 30 years, right here in Westport, Connecticut.

The IRS keeps moving whether you’re ready or not. Now is a better time than next month.

References

IRS.gov — IRS collection notice sequence, levy and garnishment procedures, Offer in Compromise eligibility guidelines, and Collection Financial Standards

IRS.gov — Substitute for Return (SFR) process documentation and taxpayer compliance requirements

IRS.gov — Enrolled Agent licensing authority and scope of representation before the IRS (Circular 230)

IRS.gov — Collection Statute Expiration Date (CSED) rules and IRS Code Section 6651 penalty provisions