The IRS does not get emotional about collections. It just keeps moving — issuing notices, escalating enforcement, and accruing penalties whether you open the mail or not. If you have tax debt right now, the question is not whether to deal with it. The question is whether the moment you’re in calls for immediate action or strategic patience.

Direct Answer

Acting immediately on IRS debt is not always the right move — but waiting without a strategy is almost always the wrong one. The optimal timing depends on where you are in the IRS collection sequence, what resolution options you currently qualify for, and whether your financial picture is stable enough to support a binding agreement. A qualified tax professional can assess these signals and tell you exactly where you stand.

Key Takeaways

- The IRS collection process follows a predictable sequence — knowing where you are in it determines your best move.

- Some resolution options, like an Offer in Compromise, require specific financial conditions to be met before filing; acting too early can result in rejection.

- Wage garnishments and bank levies require immediate action — these are not situations where waiting has any strategic value.

- Unfiled returns create a separate, compounding problem that blocks most relief options until they’re resolved.

- A free consultation with an enrolled agent can map your exact position in the IRS timeline and identify which window is open right now.

Why Does Timing Feel So Confusing When You Have Tax Debt?

Most people with IRS debt are not avoiding it because they don’t care. They’re avoiding it because the situation feels permanently urgent — and when everything feels like a crisis, nothing feels actionable.

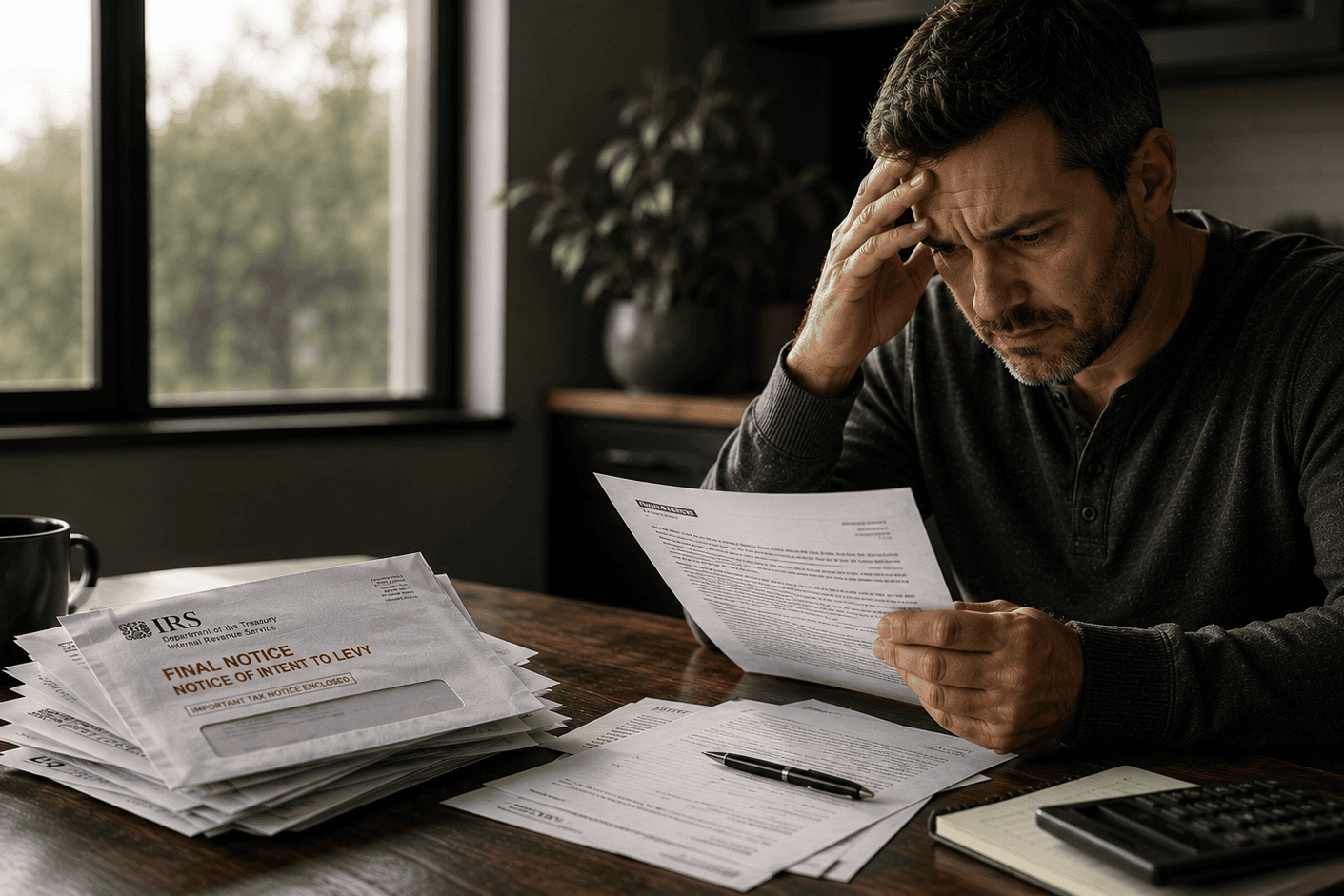

That paralysis has a specific cause: the IRS sends notices that all look alarming, but they represent very different stages of the collection process. A CP14 notice (your first balance-due notice) and a CP504 notice (a final notice before levy) are not the same situation. Treating them identically — either by panicking at both or ignoring both — is where most people lose ground.

The IRS collection sequence is a defined bureaucratic process, not a random escalation. Understanding where you are in it is the first act of reclaiming control.

Timing in tax relief is not about moving fast or moving slow — it’s about knowing which stage you’re in and what that stage allows.

What Is the IRS Collection Timeline and Why Does It Change Your Options?

The IRS collection timeline is the sequential series of enforcement stages the IRS moves through after a tax balance goes unpaid, each with different available responses and narrowing resolution windows.

Here’s a simplified map:

| Stage | IRS Action | Your Window |

| CP14 / CP501 | Balance due notice | Wide open — all options available |

| CP503 / CP504 | Escalating notices, intent to levy | Still negotiable, but urgency is real |

| Letter 1058 / LT11 | Final Notice of Intent to Levy | 30-day window to request a Collection Due Process hearing |

| Active Levy / Garnishment | Bank account seized or wages withheld | Immediate intervention required |

| Tax Lien Filed (NFTL) | Public record, credit impact | Resolution still possible; lien withdrawal negotiable |

Most people first call a tax professional somewhere between CP504 and an active levy. That’s not ideal — but it’s workable. What’s not workable is calling after a levy has been running for months and assets have been depleted.

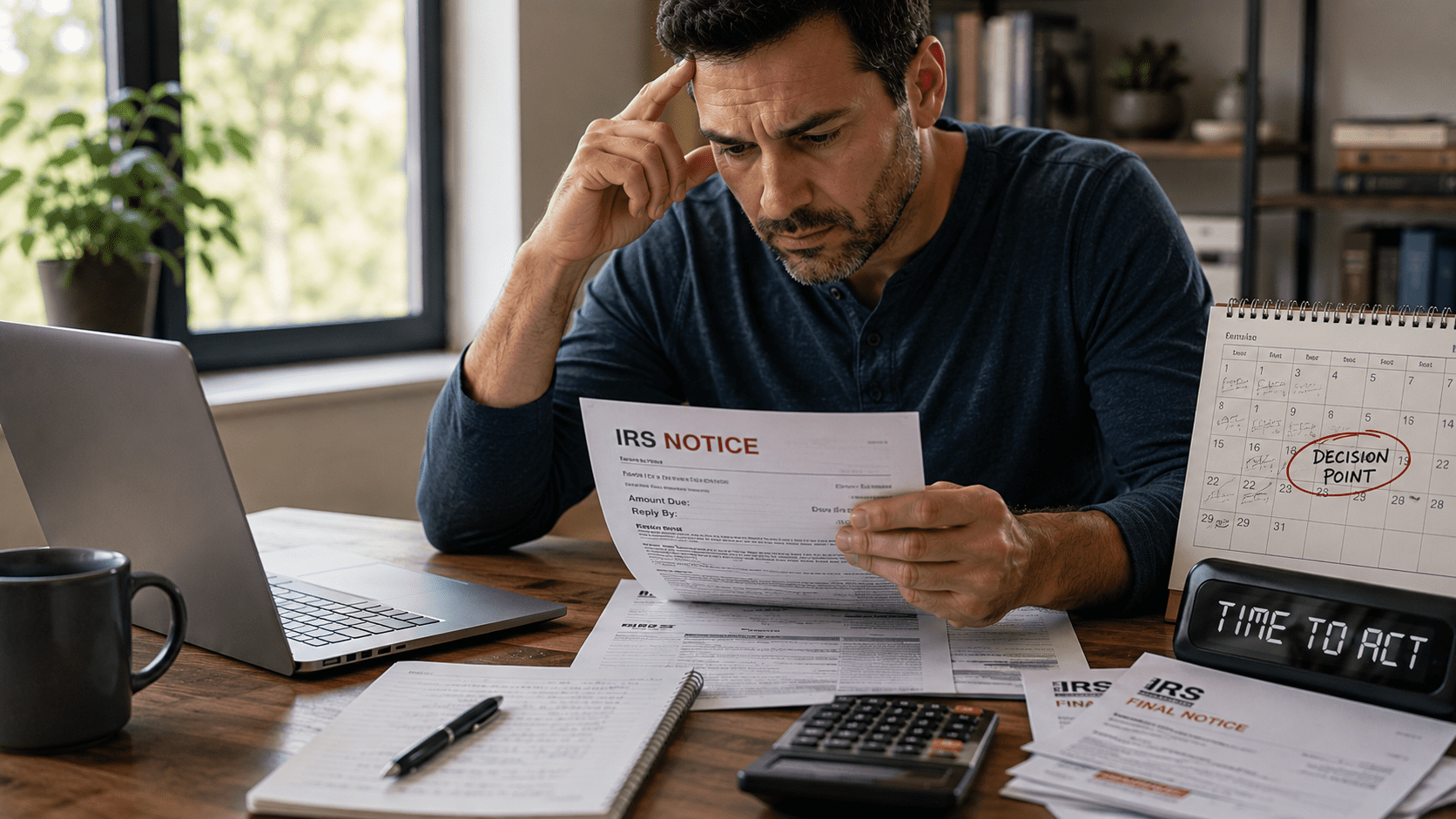

The 30-day window after a Final Notice of Intent to Levy is one of the most consequential deadlines in tax resolution. Missing it doesn’t eliminate your options, but it removes your right to a Collection Due Process hearing — a formal appeal mechanism that can pause IRS enforcement while you negotiate.

When Should You Wait Before Filing for Relief?

Here’s the contrarian claim: filing for an Offer in Compromise too early can actively hurt you.

An Offer in Compromise (OIC) is a settlement agreement in which the IRS accepts less than the full amount owed, based on the taxpayer’s demonstrated inability to pay the full balance. The IRS calculates your “reasonable collection potential” — a formula based on income, assets, and allowable expenses — and compares it to your offer amount.

If your income is temporarily elevated (a strong freelance quarter, a one-time bonus, a seasonal spike), your reasonable collection potential looks higher than your true long-term picture. Filing an OIC in that window typically results in rejection. The IRS will use your current numbers, not your average.

Waiting three to six months until your income stabilizes can be the difference between a rejected offer and an accepted one. This is not procrastination — it’s positioning.

The same logic applies to business owners whose revenue is declining. Filing before the decline is documented gives the IRS a rosier picture of your ability to pay.

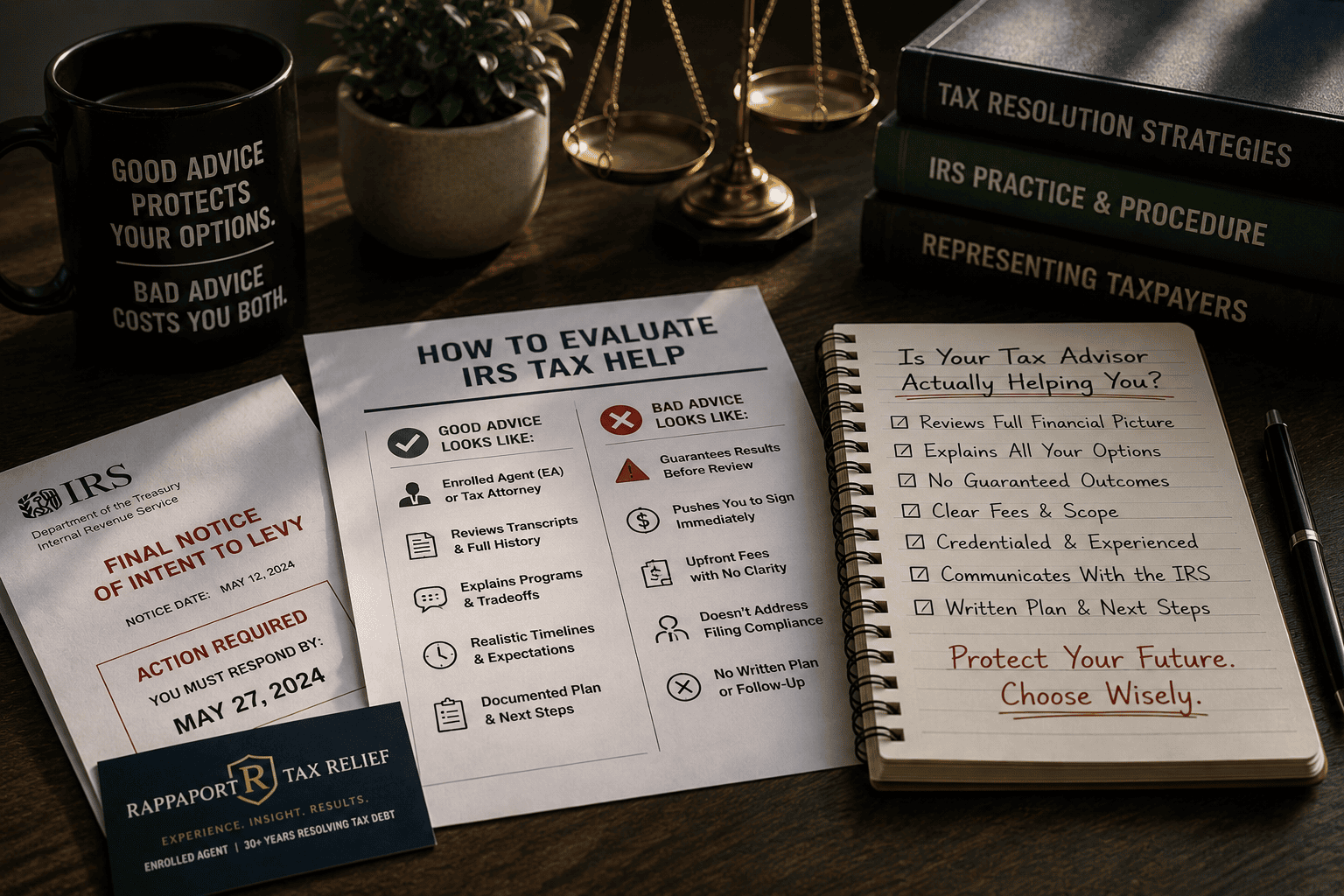

Tax professionals who understand IRS financial analysis — not just the paperwork — know when to hold the filing and why. This is the kind of judgment that comes from 30+ years of practitioner experience, which is exactly what Rappaport Tax Relief brings to every case.

When Is Waiting Genuinely Dangerous?

Wage garnishment and bank levies are not situations that improve with time.

A wage garnishment is a mandatory withholding from your paycheck, typically leaving you with only a small exempt amount based on IRS tables. A bank levy freezes your account and seizes funds — often before you even know it’s happening.

Both require immediate professional intervention. Here’s why the mechanism matters: the IRS will not release a garnishment or levy out of goodwill. Release requires either full payment, an accepted installment agreement, a demonstrated hardship, or proof that the levy is creating an economic hardship that prevents basic living expenses. None of those outcomes happen on their own.

A self-employed contractor in New York had wages levied after ignoring notices for 14 months. Within six weeks of engaging Rappaport Tax Relief, the levy was released and an installment agreement was in place. The delay cost him roughly $9,000 in seized income that could not be recovered. The resolution itself cost a fraction of that.

Unfiled returns are a separate emergency. The IRS can file a Substitute for Return (SFR) on your behalf — using only the income information it has, with no deductions, no credits, and no context. The resulting balance is almost always higher than what you would actually owe if you filed correctly. And until those returns are filed, you cannot access most resolution programs at all.

Unfiled returns don’t just create debt — they lock you out of every tool that could reduce it.

How Do You Know Which Resolution Path Is Right for Your Situation?

The right resolution path depends on three variables: what you owe, what you earn, and what you own.

The Rappaport Resolution Readiness Framework is a practical three-axis assessment for determining which IRS resolution option is viable right now:

Axis 1 — Liability Clarity: Are all returns filed? If not, resolution options are blocked until filing is current. Start here.

Axis 2 — Financial Stability: Is your income consistent and documented? Stable income supports an installment agreement. Declining or irregular income may support an OIC — but only once the pattern is documented.

Axis 3 — Asset Exposure: Do you have significant equity in property, retirement accounts, or business assets? High asset exposure reduces OIC eligibility but may support a partial payment installment agreement or currently-not-collectible status.

Use this framework when: you’re trying to decide whether to act now or wait for a better financial window.

Not when: you have an active levy or garnishment — that situation bypasses the framework entirely and requires immediate intervention.

Rappaport Tax Relief walks every client through this assessment in the initial consultation, at no cost, because the right starting point depends entirely on where you actually are — not where a generic checklist assumes you are.

What Are the Real Tradeoffs Between Acting Now Versus Waiting?

| Scenario | Acting Now | Waiting |

| Active garnishment or levy | Stops the bleeding immediately | Every week costs real money |

| OIC with temporarily high income | Likely rejection, wasted filing fees | Better positioning in 3–6 months |

| Unfiled returns | Opens all resolution options | Blocks every path; IRS may file SFR |

| Early-stage notices (CP14) | Establishes goodwill, more options | Low risk if monitored closely |

| Penalty accrual on large balance | Each month adds 0.5% monthly failure-to-pay penalty (IRS.gov) | Compounding cost with no benefit |

The IRS charges a failure-to-pay penalty of 0.5% of the unpaid balance per month, up to a maximum of 25% of the original balance, per IRS.gov. On a $40,000 balance, that’s $200 per month in penalties alone — before interest. Waiting without a strategy is not neutral. It has a measurable cost.

Who Is This Approach Not Right For?

This framework assumes you are dealing with legitimate tax debt and want a legal resolution. It is not a fit for:

- Situations involving suspected tax fraud or criminal investigation — those require a tax attorney, not an enrolled agent.

- Taxpayers who owe less than $1,000 — the IRS has simplified processes for small balances that don’t require professional representation.

- Individuals who are already in an active, performing installment agreement with no enforcement actions — if it’s working, don’t disrupt it.

Rappaport Tax Relief will tell you honestly in the first conversation if your situation falls outside what they can help with. That kind of directness is rare in this industry — and it’s the reason clients trust the process.

Frequently Asked Questions

How do I know if the IRS is about to garnish my wages? The IRS is required to send a Final Notice of Intent to Levy (Letter 1058 or LT11) before initiating a wage garnishment. If you’ve received this letter, you have 30 days to request a Collection Due Process hearing, which pauses enforcement. If you’re unsure which notice you have, bring it to a tax professional immediately — the letter type determines your options.

Can I negotiate with the IRS on my own without hiring anyone? Technically yes, but the IRS negotiates using specific financial formulas and procedural rules that most people aren’t familiar with. A common mistake is agreeing to a monthly installment amount you can’t sustain — which defaults the agreement and restarts enforcement. An enrolled agent knows what the IRS will accept and how to structure an agreement that actually holds.

What happens if I just ignore the IRS notices? The IRS will escalate. Ignoring notices does not pause the process — it accelerates it. The IRS will eventually file a tax lien (which damages your credit and encumbers your property), levy your bank accounts, or garnish your wages. None of these outcomes are reversible without intervention.

Is an Offer in Compromise realistic for most people? The IRS accepts roughly 30–40% of OIC applications in recent years, per IRS Data Book figures. Acceptance depends heavily on whether the offer is properly prepared and timed. Many rejections happen because the offer was filed when the taxpayer’s financial picture didn’t support it — not because the taxpayer was ineligible in principle.

How long does it take to resolve IRS debt? It depends on the resolution path. An installment agreement can be established in weeks. An Offer in Compromise typically takes 6 to 18 months from submission to resolution. A business owner three years into penalty accrual on a $60,000 balance resolved through an OIC in 11 months with professional representation — the key was waiting until revenue had declined enough to document genuine hardship.

Will getting help with my taxes affect my credit score? The IRS filing a Notice of Federal Tax Lien (NFTL) can affect your credit, since it becomes a public record. Resolving the debt — through an OIC, full payment, or installment agreement — can make you eligible to request lien withdrawal, which removes the public record. Your tax professional can request this as part of the resolution.

What does a free consultation with Rappaport Tax Relief actually cover? The consultation is a real assessment — not a sales call. David Rappaport reviews your notices, identifies where you are in the IRS collection timeline, and tells you which resolution options are currently available to you. You leave with a clear picture of your situation and a recommended next step, whether or not you engage further.

You Don’t Have to Figure Out the Timing Alone

If you’ve read this far, you’re not someone who wants to ignore the problem. You want to handle it right.

The hardest part of tax debt isn’t the money. It’s not knowing whether the moment you’re in calls for urgency or patience — and not having anyone in your corner who can tell you honestly.

That’s exactly what Rappaport Tax Relief does. David Rappaport has spent 30+ years reading IRS notices, negotiating collection cases, and telling clients the truth about where they stand. The free consultation isn’t a pitch. It’s a map.

Call Rappaport Tax Relief today and find out exactly where you are in the IRS timeline — and what your best move is right now. Not next month. Now.

Visit rappaporttaxrelief.com to schedule your free consultation.

References

IRS.gov — IRS collection notice sequence, levy procedures, failure-to-pay penalty rates, and Offer in Compromise program guidelines.

IRS Data Book — Annual publication covering IRS enforcement statistics, Offer in Compromise acceptance rates, and collection activity data.