The moment your employer tells you the IRS is taking a cut of your paycheck, something shifts. It’s not just the money. It’s the exposure, the helplessness, and the creeping fear that this is only the beginning.

A wage garnishment isn’t a warning. It’s the IRS already inside your finances, and it will keep taking until someone stops it.

Wage garnishment release is the formal process of getting the IRS to stop seizing a portion of your paycheck. It requires either resolving the underlying debt, entering a qualifying payment arrangement, or demonstrating hardship. And it almost always requires direct negotiation with the IRS before your next pay period. Acting fast matters because each pay cycle the garnishment runs costs you money you can’t recover.

Key Takeaways

- The IRS can garnish a far larger share of your paycheck than a private creditor. Federal consumer credit protections cap ordinary garnishments at 25% of disposable earnings, but IRS wage levies follow a different, often harsher formula

- Garnishment doesn’t stop automatically when you call the IRS. It stops when a specific release condition is met and the IRS formally notifies your employer

- The most common release paths are: installment agreement, currently-not-collectible status, offer in compromise, or demonstrated hardship

- Every pay cycle the garnishment runs is money gone permanently. There’s no refund once the IRS collects it

- Rappaport Tax Relief can intervene directly with the IRS on your behalf, often stopping garnishment faster than going it alone

Why Does the IRS Have More Power Over Your Paycheck Than a Regular Creditor?

Most people assume wage garnishment works the same way regardless of who’s collecting. It doesn’t.

Under the Consumer Credit Protection Act, Title III, private creditors are limited to garnishing 25% of your disposable earnings. Or the amount by which your earnings exceed 30 times the federal minimum wage, whichever is less. That’s the legal ceiling for most debt collectors.

The IRS doesn’t operate under that ceiling in the same way. Federal tax levies on wages follow IRS Publication 1494, which uses a table based on your filing status and number of dependents to determine the exempt amount. Whatever’s left above that exempt threshold is fair game. And for many workers, that means the IRS can take significantly more than 25%.

The practical result: a private creditor garnishment might sting. An IRS wage levy can gut a paycheck.

This is the part most people don’t realize until it’s already happening to them. The IRS isn’t bound by the same rules as a credit card company or a landlord pursuing a judgment. It has statutory collection authority that bypasses the court process entirely. Which is why it can move so fast and why stopping it requires a specific, procedurally correct response.

What Actually Triggers a Wage Garnishment. And What Comes Before It

The IRS doesn’t garnish wages without warning. What feels sudden usually isn’t.

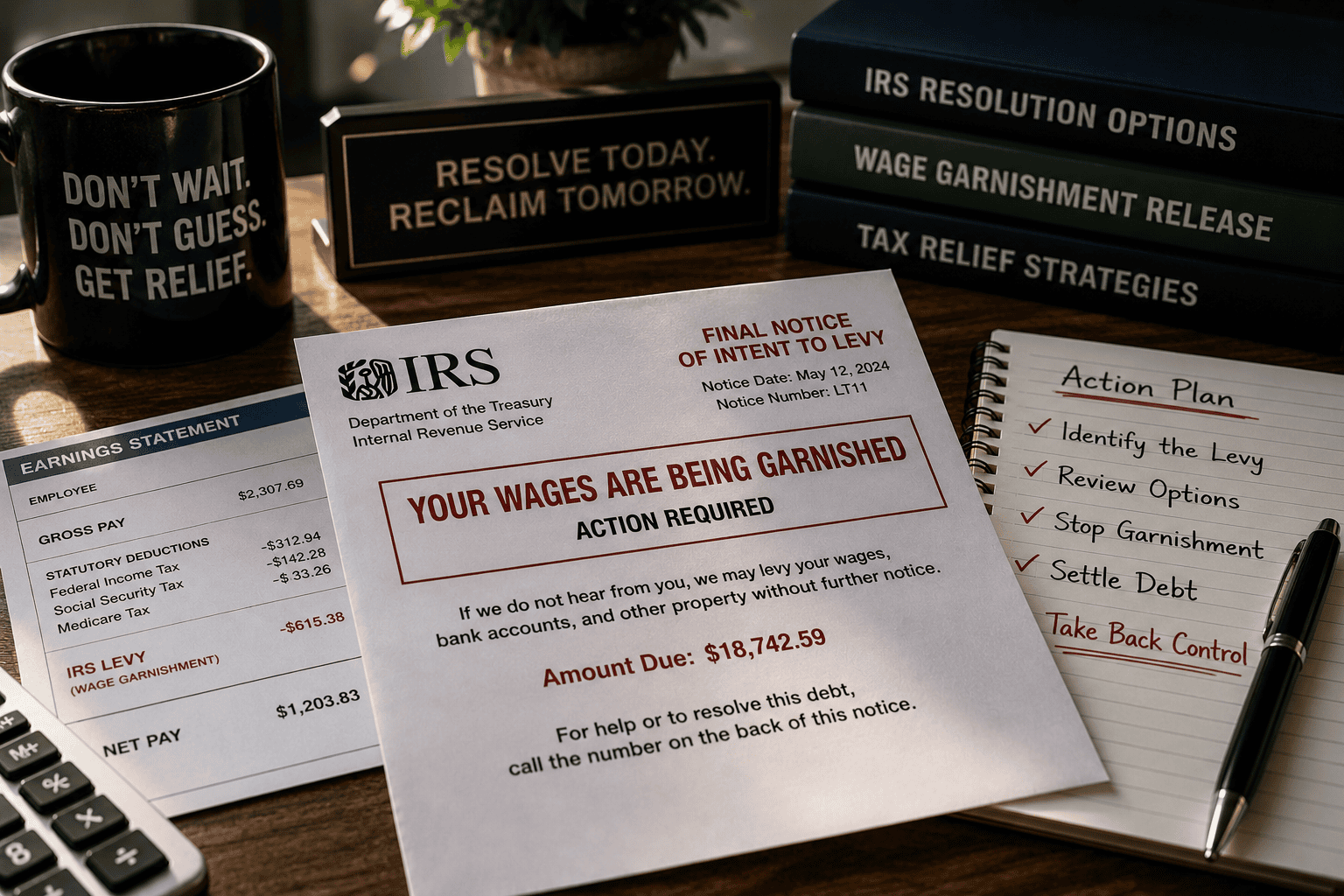

Before a levy hits your paycheck, the IRS is required to send a series of notices: a balance due notice (CP14), a demand for payment, and a Final Notice of Intent to Levy with your right to a Collection Due Process hearing. That last notice, typically an LT11 or Letter 1058, is the last formal checkpoint before enforcement begins.

Most people who end up garnished either ignored those notices, didn’t understand what they meant, or genuinely couldn’t pay and didn’t know there were options. The IRS doesn’t interpret silence as hardship. It interprets silence as an invitation to escalate.

If you’ve received a CP1058 letter or similar final notice, the window to act before enforcement is narrow. But it exists.

The Four Paths to Wage Garnishment Release

Wage garnishment release is not a single process. It’s one of four outcomes, each with different eligibility requirements and timelines.

Installment Agreement. If you can’t pay in full but can pay something, the IRS will typically release a levy once an installment agreement is in place. The IRS wants compliance more than it wants to keep garnishing. A structured installment agreement formally resolves the collection action and stops the paycheck seizure.

Currently Not Collectible (CNC) Status. If paying anything right now would leave you unable to cover basic living expenses, the IRS can classify your account as currently not collectible. This pauses collection activity, including the garnishment, while the status holds. It’s not forgiveness, but it’s breathing room.

Offer in Compromise. An offer in compromise is a negotiated settlement where the IRS agrees to accept less than the full amount owed. While an OIC is pending, collection activity is typically suspended. This is a longer process with strict eligibility requirements, but for the right situation, it can resolve the debt at a fraction of the balance.

Demonstrated Hardship or Error. If the garnishment itself was issued in error, or if it’s causing genuine economic hardship beyond normal collection standards, you can request a release on those grounds. This requires documentation and direct engagement with the IRS. It doesn’t happen by asking nicely over the phone.

The path that’s right for you depends on your income, your total balance, your filing history, and whether you have assets the IRS might pursue separately. Getting this wrong, choosing the wrong resolution path, can close off better options.

The Garnishment Resolution Framework: A Decision Map

The Levy Response Triage framework is a four-question decision tool for identifying the fastest appropriate release path before a single IRS call is made.

Use it when: you’ve received a wage levy notice or your employer has already been contacted.

- Can you pay the full balance within 120 days? If yes. A short-term payment plan stops the levy fastest.

- Can you pay something, but not the full balance? If yes. An installment agreement is the target. Hardship-based plans exist for low-income filers.

- Would any payment leave you unable to cover rent, food, or utilities? If yes. CNC status is the priority. Document your expenses first.

- Is your total debt significantly less than what you could realistically pay over your remaining earning years? If yes. An offer in compromise may be worth pursuing, but it takes longer and the garnishment may continue during review unless a separate release is negotiated.

Don’t use this framework as a substitute for professional review. Use it to walk into that first conversation knowing which direction you’re likely heading.

What Happens After the Release Is Granted?

This is the question most people don’t think to ask until they’re already in the process.

When the IRS grants a levy release, it issues a formal notice to your employer. Your employer then stops the withholding. But not immediately on the day the release is issued. There’s typically a processing lag of one to two pay cycles depending on your employer’s payroll schedule. You won’t get back what was already taken.

The garnishment release also doesn’t resolve the underlying debt. Whatever arrangement triggered the release, installment agreement, CNC status, OIC, that’s now the active obligation. If you miss a payment or fall out of compliance, the IRS can reinstate the levy without going through the full notice sequence again.

Compliance going forward isn’t optional. It’s the condition under which the release stays in effect.

This is why working with someone who manages the full picture, not just the immediate crisis, matters. Rappaport Tax Relief approaches this as a lifecycle problem: stopping the garnishment is the first step, but staying out of the IRS’s collection queue is the actual goal. You can read more about why hiring a professional for tax debt settlement matters and why the negotiation process is different when someone with standing is making the call.

Going It Alone vs. Getting Represented: The Real Comparison

The most expensive decision in a wage garnishment situation isn’t the professional fee. It’s the pay cycles lost while you figure out the process yourself.

| Situation | Going It Alone | With Rappaport Tax Relief |

| Speed to release | Slower. Learning the process while it runs | Faster. Direct IRS contact, known procedures |

| Resolution path accuracy | Risk of choosing wrong option, closing off better ones | Assessed against full picture: income, debt, filing history |

| Ongoing compliance | Easy to miss requirements, triggering reinstatement | Managed through the agreement period |

| Future exposure | Debt still exists; collection can resume | Past, present, and future tax issues addressed together |

| Cost of inaction | Every pay cycle costs real money, permanently | Professional fee is a fraction of what continued garnishment takes |

The IRS doesn’t give credit for effort. It responds to procedurally correct requests made by people who know the rules.

A Typical Garnishment Scenario

Consider a self-employed contractor in Connecticut who stopped filing for two years during a slow period, then went back to salaried work. The IRS filed substitute returns on his behalf, typically at the least favorable filing status, and assessed a balance higher than his actual liability. By the time he got an LT11 notice, the levy was already in motion.

In a case like this, the right move isn’t just stopping the garnishment. It’s filing the correct returns to replace the IRS substitutes, which often reduces the actual balance significantly, and then negotiating the resolution from that corrected number. Stopping the levy without fixing the underlying return leaves money on the table. Sometimes thousands of dollars.

The garnishment is the symptom. The unfiled or incorrect returns are the root cause.

Who This Matters Most For

Wage garnishment release is most urgent when you’re a salaried employee or W-2 contractor with no other income source. Because the garnishment hits every single pay cycle with no flexibility. It’s also critical for small business owners who pay themselves through payroll, since a levy on payroll can effectively shut down operations.

If you have unfiled returns in addition to the garnishment, what self-employed individuals in Connecticut owe the IRS is worth understanding before you make your first call. Because the sequence of steps matters, and getting it out of order can complicate the release.

This process is harder, not impossible, but harder, if you’ve already defaulted on a previous installment agreement or if there’s an active federal tax lien filed against you. Those situations require a more careful approach, but they’re not dead ends.

What Rappaport Tax Relief Does Differently

David Rappaport has spent more than 30 years as an Enrolled Agent working directly with the IRS on behalf of individuals and small businesses. Enrolled Agent status means federal authorization to represent taxpayers before the IRS at every level. Audits, appeals, collections.

The concierge approach at Rappaport Tax Relief means you’re not handed off to a case manager after the intake call. David works your case personally. That matters in garnishment situations because the IRS responds to representatives who know the file. Not to someone reading from a script.

The goal isn’t just the release. It’s getting you to a place where the IRS isn’t a recurring crisis in your life.

Frequently Asked Questions

How fast can a wage garnishment actually be stopped?

It depends on the resolution path and how quickly documentation is assembled, but once an installment agreement or hardship determination is in place, the IRS is required to release the levy. Your employer then needs a processing cycle to implement it. Realistically, a few weeks from first contact to cleared paycheck is possible. But only if the process moves without delays.

Will my employer know why my wages are being garnished?

Yes. The IRS sends the levy notice directly to your employer’s payroll department, and it specifies that it’s a federal tax levy. Your employer is legally required to comply and is not permitted to fire you solely because of a single garnishment. But they will know.

Can the IRS garnish my wages if I’m self-employed or a freelancer?

Not through payroll. But the IRS can levy your bank accounts, seize accounts receivable, and intercept payments from clients. The mechanism is different, but the effect is the same. Self-employed individuals face a different collection exposure that requires a different response strategy.

What if I can’t afford to pay anything at all right now?

Currently Not Collectible status exists specifically for this situation. If your basic living expenses consume your income, the IRS can suspend collection activity. It doesn’t erase the debt, but it stops the garnishment and gives you time to stabilize. You’ll need to document your financial situation thoroughly.

Does filing for bankruptcy stop a wage garnishment?

An automatic stay triggered by bankruptcy filing does halt most IRS collection activity temporarily, including wage levies. But bankruptcy has significant long-term consequences and doesn’t discharge most federal tax debt. It’s a serious option that requires careful analysis. Not a quick fix.

What happens if I ignore the garnishment and just let it run?

The IRS keeps taking until the debt is paid in full, or until you take action. There’s no point at which it stops on its own. Every pay cycle that passes is money permanently gone, and the underlying penalties and interest continue to accumulate on any remaining balance.

How is Rappaport Tax Relief different from a national tax relief company?

National firms typically use a volume model. Intake teams, case managers, and limited access to the person actually negotiating. Rappaport Tax Relief is a concierge practice led by David Rappaport personally. You work directly with the Enrolled Agent handling your case, not a support staff layer. For people in Connecticut and the surrounding region, that direct relationship changes the quality of the representation.

The Next Step Isn’t Complicated

If your wages are being garnished right now, or if you’ve received a final notice and haven’t responded yet, the most important thing you can do is talk to someone who can assess your actual options. Not a general overview, but your specific situation, your balance, your filing history, your income.

Rappaport Tax Relief offers a free consultation. Not a sales call. A real conversation about where you stand and what the realistic paths forward look like. Call before your next pay cycle runs.

About the Author

Rappaport Tax Relief is a tax resolution practice based in Westport, Connecticut, specializing in IRS debt negotiation, wage garnishment release, and comprehensive tax problem resolution. Led by Enrolled Agent David Rappaport with more than 30 years of hands-on experience, the firm works directly with individuals, self-employed professionals, and small business owners facing IRS collection activity, unfiled returns, and accumulated tax debt. Rappaport Tax Relief serves clients throughout Connecticut and the surrounding region with a concierge approach that addresses past, present, and future tax issues under one roof.

References

U.S. Consumer Credit Protection Act, Title III. Wage garnishment limits for ordinary creditors and support obligations