The Most Common Tax Debt Mistakes. And Why Smart People Keep Making Them

The letters have been sitting on the counter for weeks. You know what they say, roughly, but opening them feels like pulling a pin on something you're not ready to handle. That gap. Between knowing something is wrong and doing something about it. Is where most tax debt situations go from manageable to serious.

The most common tax relief mistakes aren't made by careless people. They're made by people who are stressed, busy, and working with incomplete information about how IRS collections actually work.

Key Takeaways

- Waiting to respond to IRS notices doesn't pause the collection process. It accelerates it

- Unfiled returns create a separate, compounding problem that must be resolved before any payment arrangement can be negotiated

- The IRS's own installment agreement isn't always the best deal available. A qualified representative can often negotiate better terms

- Responding to the IRS without professional representation is the single most common way people accidentally waive their rights or lock in unfavorable agreements

- Penalty abatement is a legitimate, underused tool. Most people don't know to ask for it

Why Does Waiting Feel Like a Strategy When It Isn't?

Silence from the IRS feels like a reprieve. It isn't.

The IRS collection process runs on a defined sequence of notices, CP14, CP501, CP503, CP504, and eventually LT11 or CP1058, each one escalating toward enforcement action. The sequence doesn't pause because you haven't responded. It just keeps moving, automatically, until a levy or garnishment is issued.

The mechanism here matters: a bank levy isn't a decision someone at the IRS makes about you specifically. It's a bureaucratic output. Once the notice sequence completes without a response, enforcement is triggered without a human being actively choosing to target you. That's why waiting feels passive but actually accelerates the timeline toward the worst outcomes.

A typical case looks like this: someone receives a CP14 notice (the first balance-due letter), sets it aside intending to deal with it later, and receives no further notices for several months. Because they've moved and the IRS has an old address. The first sign that anything has escalated is a call from their employer about a wage garnishment. By that point, the IRS has already filed a federal tax lien, and the window for certain resolution options has narrowed significantly.

If you've received an IRS notice and aren't sure what it means or what comes next, understanding how to respond to a CP14 notice is a practical starting point. The response window is shorter than most people expect.

What Happens When You File a Payment Plan Without Checking Your Options First?

Most people who contact the IRS directly end up in a standard installment agreement. That's not always wrong. But it's often not the best available outcome.

The IRS offers several resolution pathways, and the one you land in depends almost entirely on what you ask for and how you present your financial information. The standard installment agreement is the default. It's easy to get approved for, which is exactly why it's often the most expensive long-term choice.

Here's what most people don't know: the IRS also offers Currently Not Collectible (CNC) status, Partial Pay Installment Agreements (PPIAs), and Offer in Compromise (OIC) arrangements. Each with different qualification thresholds, different effects on penalties and interest, and different implications for how long the IRS can legally pursue the debt.

Penalty abatement is another tool that goes almost entirely unused by people who represent themselves. The IRS's First-Time Penalty Abatement policy allows qualified taxpayers to have certain penalties removed. But you have to request it, and you have to request it correctly. Most people don't know it exists.

Accepting the first payment option the IRS offers is the financial equivalent of paying sticker price when there was a negotiated rate available the whole time.

The Unfiled Returns Problem: Why It Has to Come First

Unfiled returns aren't just a separate issue from tax debt. They're a prerequisite problem. The IRS won't negotiate a payment arrangement, approve an Offer in Compromise, or release a levy on a taxpayer who has outstanding unfiled returns. The resolution process can't start until the filing record is current.

This creates a specific trap: people who owe money and also have unfiled years sometimes focus all their energy on the debt they know about, while the unfiled years sit in the background quietly generating additional liability, penalties, and interest. By the time they try to enter a formal resolution program, they're dealing with a larger, more complex problem than they started with.

Getting current on filings isn't just paperwork. It's the entry ticket to every resolution option the IRS offers.

If you're self-employed and dealing with both unfiled returns and accumulated debt, the compounding effect is usually worse - self-employed taxpayers in Connecticut face a specific set of IRS debt dynamics that are worth understanding before you take any action.

The "I'll Handle It Myself" Calculation. What It Actually Costs

There's a real argument for handling straightforward tax matters without professional help. A simple return, a single-year balance you can pay in full, a first-time penalty abatement request with a clean filing history. These are situations where the stakes are lower.

But the calculation changes completely when enforcement has started, when multiple years are involved, when you're self-employed with complex income, or when the IRS has already filed a lien or issued a levy. At that point, the question isn't whether professional representation costs money. It's whether the cost of making the wrong move. Locking in a bad agreement, missing a qualification window, or inadvertently waiving appeal rights. Exceeds the cost of getting qualified help.

It almost always does.

The IRS negotiates with enrolled agents and tax professionals every day. They know the process, the thresholds, and the available pathways. A taxpayer calling on their own behalf, without that knowledge, is at a structural disadvantage. Not because the IRS is adversarial, but because information asymmetry is built into the system.

The Resolution Pathway Comparison

| Approach | Typical Outcome | Key Risk |

| Ignoring IRS notices | Levy, garnishment, lien | Enforcement triggers automatically |

| DIY installment agreement | Standard terms, full balance owed | Misses better options; no penalty abatement |

| National tax relief mill | Variable; high upfront fees | Lack of personalized attention; frequent complaints |

| Qualified enrolled agent representation | Negotiated terms, penalty review, full option assessment | Requires honest financial disclosure |

Rappaport Tax Relief works through the full option set before recommending a resolution path. Not because it's more complicated, but because the difference between the right agreement and the default one can be measured in thousands of dollars.

The "Fresh Start" Framing Mistake

The IRS's Fresh Start Initiative. A set of expanded eligibility criteria for installment agreements and Offer in Compromise. Is real and useful. But it's also become a marketing phrase that some national tax relief firms use to imply they have access to special programs that others don't.

They don't. The Fresh Start Initiative is a public IRS policy. What differs between providers is how well they document your financial position, how accurately they calculate your Reasonable Collection Potential (RCP). The IRS's formula for determining what you can realistically pay. And how effectively they present your case.

RCP is the key variable in an Offer in Compromise. It's calculated from your income, allowable expenses, asset equity, and remaining collection statute period. A miscalculation in either direction. Overstating your ability to pay, or understating it in ways the IRS will reject. Can sink an OIC that should have been approved, or leave money on the table in a settlement that could have been lower.

The most confident pitch is often the least trustworthy signal. A firm that guarantees approval before reviewing your financials doesn't understand the process. Or is counting on you not to.

Who This Approach Matters Most For

Tax resolution isn't a one-size outcome. The strategies that work for a salaried employee with a single year of unpaid taxes are different from what works for a small business owner with three years of unfiled returns, payroll tax liability, and a pending bank levy.

Rappaport Tax Relief's approach is built around the specific situation. Not a templated program. That matters most when the stakes are high: active enforcement, multiple years of debt, business tax issues, or situations where the wrong move forecloses a better option permanently.

If you're facing a wage garnishment and don't know what your options are, understanding what to do when the IRS is garnishing your wages is the time to act before the next pay period. Not after.

FAQ

How long does it actually take to resolve IRS tax debt?

It depends on the resolution path. A straightforward installment agreement can be set up in weeks. An Offer in Compromise typically takes six to twelve months for IRS review and decision. Cases involving unfiled returns take longer because the filing record has to be brought current before formal negotiations can begin.

Can the IRS really take money directly from my bank account?

Yes. A bank levy allows the IRS to seize funds directly from your account. Typically with a 21-day holding period before the funds are transferred, which is the window to challenge or negotiate a release. Once that window closes, the money is gone. A levy can be released, but it requires immediate action and documentation of your financial hardship or a payment arrangement.

What's the difference between an enrolled agent and a tax attorney?

An enrolled agent is a federally licensed tax professional authorized to represent taxpayers before the IRS in all matters. Audits, collections, appeals. A tax attorney has legal training and can handle litigation if a case goes to court. For most IRS collection and resolution cases, an enrolled agent with deep IRS negotiation experience is the right fit. Rappaport Tax Relief is led by Enrolled Agent David Rappaport with more than 30 years of hands-on practice.

Will an Offer in Compromise hurt my credit?

An OIC itself doesn't appear on your credit report. A federal tax lien, which the IRS may file before an OIC is submitted, does affect your credit. Resolving the underlying tax debt is the path to getting a lien released, which is part of what a complete resolution process addresses.

What if I can't afford to pay anything right now?

Currently Not Collectible (CNC) status is a formal IRS designation for taxpayers who genuinely can't meet basic living expenses and pay their tax debt simultaneously. It doesn't eliminate the debt, but it pauses active collection while your financial situation is on record. It's a legitimate option that most people don't know to ask for.

What happens if I just keep ignoring the IRS?

The collection sequence continues automatically. The IRS will file a federal tax lien, issue levies against your bank accounts, and garnish your wages. All without needing a court order. The collection statute of limitations is generally ten years from the date of assessment, so the IRS has time and tools on its side. Waiting doesn't make the problem smaller.

How do I know if I qualify for penalty abatement?

The IRS's First-Time Penalty Abatement policy applies to taxpayers with a clean three-year filing and payment history before the year in question. There's also reasonable cause abatement for documented circumstances like illness, natural disaster, or reliance on professional advice. Most people who qualify never claim it because they don't know to ask. A qualified representative reviews this as part of the full resolution process.

Stop Waiting for the Right Moment. There Isn't One

The IRS doesn't wait. Its collection process runs on its own clock, and every week without a response is a week closer to enforcement. If you've been putting this off because it feels overwhelming or you're not sure where to start, that's exactly the state Rappaport Tax Relief is built to help you through.

Call for a free consultation. Not to commit to anything. Just to understand what you're actually dealing with, what options are available, and what the next step looks like. That clarity alone is worth more than another week of waiting.

About the Author

Rappaport Tax Relief is a tax resolution firm based in Westport, Connecticut, specializing in IRS debt negotiation, penalty abatement, and comprehensive tax problem resolution. Led by Enrolled Agent David Rappaport with more than 30 years of experience, they work with individuals, self-employed professionals, and small business owners across the New York and New England area to resolve past tax debt, address active IRS enforcement, and prevent future problems through personalized, concierge-level service.

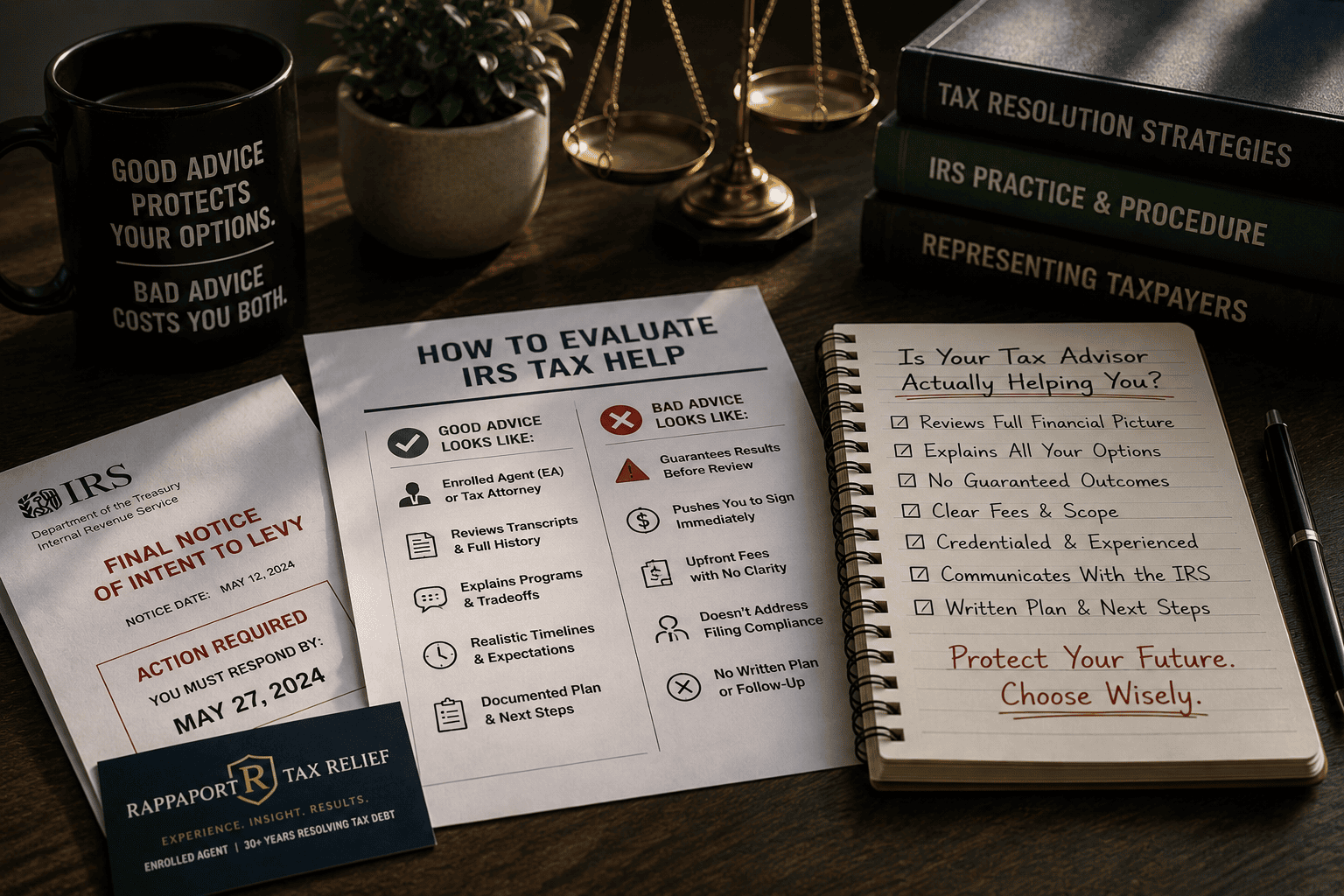

How to Tell If Your Tax Relief Advice Is Actually Helping You. Or Making Things Worse

The feeling that you're finally doing something about your IRS problem can be just as dangerous as doing nothing. When you're overwhelmed and desperate for a way out, the wrong guidance doesn't just fail to help. It actively narrows the options that remain.

Bad IRS assistance is everywhere. And it often sounds exactly like good IRS assistance.

Credible IRS assistance means a qualified professional. An Enrolled Agent, tax attorney, or CPA with demonstrated resolution experience. Reviews your full financial picture, identifies every resolution program you qualify for, and communicates directly with the IRS on your behalf. It results in a documented plan with realistic outcomes, not promises. The alternative is often a sales pitch dressed up as advice.

Key Takeaways

- The most confident pitch is usually the least trustworthy signal. Legitimate practitioners explain options and tradeoffs, not guaranteed outcomes

- Upfront fees with no clear scope of work are a structural warning sign, not just a red flag

- An Enrolled Agent (EA) is federally licensed to represent taxpayers before the IRS. That credential means something specific and verifiable

- Waiting to find "better" help is itself a decision, and it's usually the most expensive one you'll make

- Real IRS assistance addresses your past filings, your current debt, and your future compliance. Not just the immediate crisis

Why Does Bad Tax Relief Advice Feel Credible Until It Isn't?

The tax relief industry has a predatory fringe, and it survives because the people it targets are already frightened. When you're facing a wage garnishment or a bank levy, your threshold for hope drops. Someone who sounds authoritative and tells you what you want to hear. That your debt can be settled for pennies on the dollar, that the IRS will back off, that this is simple. Gets hired.

The mechanism isn't stupidity. It's information asymmetry. You don't know what the IRS will actually accept, what programs you qualify for, or what a realistic outcome looks like. Predatory firms exploit that gap deliberately.

The most confident pitch is usually the least trustworthy signal. Legitimate practitioners explain options and tradeoffs. They tell you what might not work. They don't promise outcomes the IRS hasn't agreed to.

What Does Credible IRS Assistance Actually Look Like?

Credible IRS assistance starts with a full financial disclosure. Income, assets, liabilities, filing history. Not a phone call where someone asks how much you owe and then tells you they can fix it.

A qualified practitioner will pull your IRS transcripts to see what the agency actually has on file. This step alone changes everything. What you think you owe and what the IRS has assessed are sometimes two different numbers. Unfiled returns create estimated assessments that are almost always higher than the real liability.

From there, a real professional maps your situation to the available resolution programs: an installment agreement if you can pay over time, an Offer in Compromise if your income and assets genuinely support a reduced settlement, Currently Not Collectible status if you can't pay anything right now, or penalty abatement if you qualify. If you want to understand what qualifying for an Offer in Compromise actually requires, the criteria are specific. It's not a blanket program, and not everyone qualifies.

The process takes time. Honest practitioners say so.

The Credential Gap: Why "Tax Expert" Means Nothing on Its Own

Anyone can call themselves a tax expert. The title isn't regulated.

Three credentials actually matter for IRS representation:

- Enrolled Agent (EA): Federally licensed by the IRS to represent taxpayers in all matters. Audits, collections, appeals. The EA designation requires passing a rigorous three-part exam covering individual and business tax, and passing an IRS background check. It's the only credential issued directly by the IRS.

- Tax Attorney: Licensed to practice law with specific tax expertise. Valuable in complex situations involving fraud allegations, Tax Court proceedings, or criminal exposure.

- CPA with resolution experience: Certified Public Accountants can represent clients before the IRS, but not all CPAs specialize in resolution work. The credential alone doesn't confirm the experience.

David Rappaport at Rappaport Tax Relief is an Enrolled Agent with more than 30 years of hands-on resolution experience. That combination. Federal licensure plus three decades of actual IRS negotiation. Is the difference between someone who knows the rules and someone who knows how the IRS behaves in practice.

The Five Warning Signs Framework: Spotting Bad Advice Before It Costs You

The Five Warning Signs Framework is a pre-engagement filter. A set of observable behaviors that signal a provider is selling, not advising. Use it before you sign anything.

Warning Sign 1. Guaranteed outcomes before reviewing your financials. The IRS decides what it accepts. No one can guarantee a settlement amount before seeing your income, assets, and filing history. Anyone who does is lying.

Warning Sign 2. Upfront fees with no defined scope. Legitimate firms charge for defined services. A vague retainer with no written explanation of what's included is a structural warning, not just a communication style.

Warning Sign 3. Pressure to act immediately. Real IRS deadlines exist, but they're specific and documentable. If someone's urgency is about closing the sale rather than a real statutory deadline, that urgency is manufactured.

Warning Sign 4. No mention of your filing compliance. You can't resolve a collection problem while leaving unfiled returns on the table. The IRS won't accept a resolution agreement from someone who hasn't filed. Any adviser who skips this conversation isn't doing the job.

Warning Sign 5. No direct access to the person working your case. National tax relief mills often take your money and hand your file to a junior associate you've never spoken to. You deserve to know who's representing you and be able to reach them.

What Happens When You Wait?

Consider a typical scenario: a self-employed contractor in Connecticut receives a CP14 notice. The IRS's first formal balance-due letter. He sets it aside, tells himself he'll deal with it when things slow down. Three months later, he gets an LT11 letter, which is a final notice of intent to levy. At that point, the IRS can move against his bank account or his clients' payments to him. The window for certain resolution options has narrowed. The stress has compounded.

This is the structural problem with waiting. It doesn't feel like a decision. But the IRS doesn't pause because you're busy. If you've received an LT11 letter, understanding what that notice triggers and how fast the timeline moves is information you need immediately.

Waiting is the most expensive move most people make. Not because the debt grows (though it does, with penalties and interest), but because resolution options that exist today don't always exist in six months.

What Rappaport Tax Relief Does Differently

The concierge model isn't a marketing phrase. It describes a specific structure: you work directly with David Rappaport, not a case manager who's never spoken to the IRS on your behalf. Your situation gets individual attention, not a workflow.

Rappaport Tax Relief addresses three time horizons at once. The past (unfiled returns, prior year debt), the present (active levies, garnishments, notices), and the future (staying compliant so this doesn't happen again). Most firms focus only on the immediate crisis. That leaves the root cause intact.

For anyone facing a bank levy specifically, the process of stopping an IRS levy involves specific procedural steps that have to happen in the right order and on the right timeline. Getting that wrong doesn't just delay relief. It can eliminate it.

The firm is based in Westport, Connecticut, and serves individuals and small business owners throughout the New York and Connecticut area.

Who This Matters Most For

This level of representation matters most when:

- You have multiple years of unfiled returns

- The IRS has already issued a levy or garnishment

- You're self-employed with inconsistent income that complicates standard payment calculations

- You've already tried to handle this yourself and the IRS hasn't responded or has escalated

If your situation is a single year of debt with no collection action and a straightforward income picture, the stakes are lower. But if any of the above applies to you, the cost of the wrong adviser, or no adviser, is almost always higher than the cost of qualified help.

Comparison: Acting With Qualified Help vs. Going It Alone

| Situation | With Rappaport Tax Relief | Without Qualified Help |

| Levy or garnishment in place | Immediate representation, procedural steps to request release | No one communicating with IRS; levy continues |

| Unfiled returns | Transcripts pulled, returns prepared, compliance restored before resolution begins | IRS estimates create inflated liability; resolution blocked |

| Offer in Compromise eligibility | Full financial analysis determines real qualification | DIY applications frequently rejected without knowing why |

| Ongoing compliance | Future filings managed, no recurrence | Same problem resurfaces within 1-2 years |

| Access to practitioner | Direct access to David Rappaport | National mills: case handed to junior staff |

FAQ

How do I know if a tax relief company is legitimate? Check whether the person representing you holds a verifiable credential. Enrolled Agent, CPA, or tax attorney. Look them up through the IRS's Preparer Tax Identification Number database or your state's licensing board. If they can't name the specific person handling your case or won't put the scope of work in writing, walk away.

Can the IRS really garnish my wages without warning? Not without notice. But the notices come earlier in the process than most people realize. The LT11 or Letter 1058 is the final notice before levy action. By the time that arrives, the IRS has already sent multiple prior notices. If you've been setting letters aside, you may be closer to enforcement than you think.

What's the difference between an Offer in Compromise and an installment agreement? An Offer in Compromise is a settlement. You pay less than the full amount owed, and the IRS accepts it as full resolution. An installment agreement is a payment plan for the full liability over time. The OIC requires demonstrating that your income and assets genuinely can't support full repayment. Not everyone qualifies, and the application process is detailed.

Is it too late to get help if the IRS has already levied my bank account? No, but the timeline matters. A levy can be released if you act quickly and meet specific conditions. The longer funds sit under a levy, the harder reversal becomes. This is exactly the kind of situation where direct representation, not a phone call to the IRS yourself, makes the difference.

Why do I need to file unfiled returns before resolving my debt? The IRS won't finalize any resolution agreement, installment plan, OIC, or otherwise, while returns are outstanding. It's a hard requirement. Getting into compliance first isn't a delay; it's a prerequisite. A practitioner handles both simultaneously rather than sequentially, which saves time.

What does a free consultation actually tell me? A real consultation should tell you which resolution programs you likely qualify for, what the IRS has on file, and what the process looks like from here. If the consultation is mostly a sales call with no substantive analysis of your situation, that's information about how the firm operates.

How long does tax resolution actually take? It depends on the resolution path. An installment agreement can be established relatively quickly once you're in compliance. An Offer in Compromise typically takes several months to process after submission, and the IRS can request additional documentation. There's no honest single answer. Anyone who gives you a specific timeline before reviewing your case is guessing or selling.

You Already Know Something Is Wrong. That's Why You're Here

The worst part of a tax problem isn't the number. It's the feeling that you don't know what happens next, who's actually on your side, or whether the advice you're getting is real.

If you've been sitting on IRS notices, if a levy or garnishment has already started, or if you've talked to someone who made promises that felt too clean. This is the moment to get a second opinion from someone who'll tell you the truth about where you stand.

Rappaport Tax Relief offers a free consultation. Not a sales call. An actual conversation about your situation, your options, and what realistic resolution looks like for you specifically. Call and talk to David Rappaport directly. The person who will actually work your case.

About the Author

Rappaport Tax Relief is a tax resolution firm based in Westport, Connecticut, specializing in IRS debt negotiation, levy and garnishment release, unfiled return resolution, and long-term tax compliance. Led by Enrolled Agent David Rappaport with more than 30 years of hands-on experience, the firm serves individuals and small business owners throughout the Connecticut and New York area who need direct, personal representation. Not a case number in a national call center.

Tax Relief in 2026: What's Actually Working Now (And What Isn't)

The IRS collected more than $98 billion in enforcement revenue in a recent fiscal year, and that number keeps climbing. If you're carrying tax debt right now, you're not dealing with a slow-moving bureaucracy. You're dealing with a machine that doesn't pause, doesn't negotiate on its own, and doesn't care that you didn't understand what you owed.

Tax relief in 2026 looks different than it did five years ago. Some resolution paths have opened up. Others have quietly closed. Knowing which is which could be the difference between a manageable payment plan and a bank levy that empties your account on a Tuesday morning.

Direct Answer

Tax relief still works in 2026. But the strategies that produce results have shifted. Offer in Compromise acceptance remains selective, installment agreements are more accessible than most people realize, and IRS enforcement has accelerated after years of staffing rebuilds. The taxpayers who get the best outcomes are those who act before the IRS escalates, not after.

Key Takeaways

- Offer in Compromise is not a universal fix. It works for a specific financial profile, and most people who apply without professional help get rejected

- Installment agreements are currently one of the most reliable resolution tools for moderate debt, but the terms you negotiate upfront determine how painful the next few years feel

- IRS enforcement timelines have shortened. Wage garnishments and bank levies are arriving faster than they were two years ago

- Penalty abatement is one of the most underused relief options available, and it requires no special financial hardship to qualify

- Waiting to act is not a neutral choice. Every month of inaction adds interest, compounding penalties, and narrows the resolution options still available to you

What Has Actually Changed About Tax Relief in 2026?

The IRS isn't the same agency it was in 2021. After years of understaffing and pandemic-era collection pauses, enforcement capacity has been rebuilt. The LT11 letters are going out faster. The CP14 notices are following up sooner. The gap between "first notice" and "levy action" has compressed.

What this means practically: the window to resolve a tax problem before it becomes a collection crisis is shorter now than it's been in years.

For taxpayers in Connecticut and the broader New England area, this shift is real and measurable. Practitioners who work IRS cases daily are seeing faster escalation timelines and less tolerance for informal delays.

The core resolution tools haven't changed. Offer in Compromise, installment agreements, Currently Not Collectible status, penalty abatement. But the conditions under which each one works have shifted. Here's what's actually working now.

What's Working: The Resolution Tools With Real Traction Right Now

- Streamlined Installment Agreements

For taxpayers who owe under $50,000 and have filed all required returns, streamlined installment agreements remain one of the most accessible and reliable paths to resolution. The IRS approves these without requiring a full financial disclosure, which speeds up the process considerably.

The catch most people miss: the monthly payment amount matters enormously. If you accept the IRS's initial payment proposal without negotiating, you may lock yourself into terms that strain your budget for years. A qualified representative can push back on that number using allowable expense standards. And often get it reduced.

If you're wondering how installment agreements for federal income taxes actually work in practice, the mechanics matter as much as the eligibility.

- Penalty Abatement. Especially First-Time Abatement

First-Time Abatement (FTA) is the IRS's own program for removing penalties from taxpayers who have a clean compliance history. If you've filed and paid on time for the three years before the year in question, you may qualify to have failure-to-file or failure-to-pay penalties removed entirely.

Most people don't know this exists. The IRS doesn't advertise it. And it doesn't require financial hardship. Just a clean prior record.

This is one of the most underused tools in tax resolution, and it can eliminate thousands of dollars in penalties without the complexity of an Offer in Compromise.

- Currently Not Collectible (CNC) Status

If your income genuinely doesn't cover basic living expenses after the IRS's own allowable expense calculations, you may qualify for CNC status. The IRS temporarily suspends collection activity, no levies, no garnishments, while your account sits in this status.

It's not permanent, and interest continues to accrue. But for someone in a genuine financial crisis, it buys time to stabilize without the threat of enforcement action overhead.

- Offer in Compromise. For the Right Profile

Offer in Compromise (OIC) is the most talked-about tax relief tool and the most misunderstood. An OIC is a settlement where the IRS agrees to accept less than the full amount owed. But only when it calculates that you genuinely can't pay the full balance over the remaining collection statute.

The IRS's acceptance rate for OICs is not high. The taxpayers who succeed are those whose Reasonable Collection Potential, the IRS's formula for what you can realistically pay, actually comes in below what they owe. If you want to understand whether you might qualify, the OIC eligibility criteria in Connecticut lay out the key factors clearly.

What Has Stopped Working (Or Never Worked the Way People Think)

Ignoring IRS notices and hoping the problem resolves itself.

It won't. The IRS doesn't forget. It doesn't get tired. And every month you wait, the penalty and interest balance grows. Failure-to-pay penalties accrue at 0.5% per month on the unpaid balance. That's not catastrophic on its own. But compounded over two or three years, it adds up to a debt that's meaningfully larger than what you originally owed.

DIY Offer in Compromise submissions.

The IRS's OIC pre-qualifier tool gives people false confidence. Calculating Reasonable Collection Potential correctly requires knowing which expense allowances apply to your situation, how to value assets the IRS will scrutinize, and how to present your financial picture in a way that supports your case. A rejected OIC doesn't just waste time. It can reset the collection clock and signal to the IRS that you have assets worth pursuing.

Hiring a national tax relief firm based on a late-night TV ad.

This is where real damage happens. Predatory firms exploit the information gap between what taxpayers know and what the IRS process actually requires. They collect large upfront fees, make promises about settlements they can't guarantee, and then disappear or produce nothing. The FTC has taken action against multiple national firms for exactly this pattern.

The most confident pitch is often the least trustworthy signal.

The Resolution Decision Matrix: Which Path Fits Your Situation?

Use this framework, call it the Tax Debt Triage Model, to identify which resolution path matches your actual circumstances. It's not a substitute for professional analysis, but it helps you understand the landscape before your first conversation.

| Your Situation | Most Likely Path | What to Watch For |

| Owe under $50K, all returns filed | Streamlined Installment Agreement | Negotiate payment amount. Don't accept the IRS's first proposal |

| Clean prior compliance history | First-Time Penalty Abatement | Apply before paying. Approval removes the penalty, not just defers it |

| Income below IRS expense allowances | Currently Not Collectible status | Temporary. Reassessed annually; interest still accrues |

| Low income, few assets, large debt | Offer in Compromise | Requires full financial disclosure; rejection is common without professional help |

| Unfiled returns + active enforcement | File first, then resolve | Can't negotiate while non-compliant. Filing is the prerequisite |

| Wage garnishment already active | Immediate representation needed | Garnishments can be released, but timing and documentation matter |

Why Going It Alone Costs More Than It Saves

Here's the contrarian truth most people don't want to hear: the cost of professional representation is almost always smaller than the cost of a mistake made without it.

Consider a typical case: a self-employed contractor in Connecticut owes $28,000 in back taxes across three years. He files his own OIC, underestimates his Reasonable Collection Potential by failing to account for a vehicle the IRS values differently than he does, and gets rejected. The IRS now has a fuller picture of his finances and begins levy proceedings. What could have been a negotiated installment agreement at a manageable monthly payment becomes a bank levy and a much harder negotiation from a weaker position.

The mechanism here isn't complexity. It's information asymmetry. The IRS knows its own formulas. Most taxpayers don't. A representative who works these cases every day closes that gap.

Rappaport Tax Relief, based in Westport, Connecticut, operates on exactly this principle. David Rappaport has spent 30+ years working IRS cases directly. Not delegating them to junior staff, not running a volume-based call center. If you're dealing with a wage garnishment that's already started, that kind of direct attention isn't a luxury. It's what determines whether the garnishment gets released or drags on for months.

Who Gets the Best Outcomes From Tax Relief. And Who Doesn't

Tax relief works best when you act before the IRS escalates to enforced collection. The further along the enforcement chain you are, from notice to lien to levy to garnishment, the fewer options remain and the harder each one is to execute.

It works least well when:

- Returns are still unfiled (you can't negotiate while non-compliant. Filing is the prerequisite for everything else)

- The taxpayer has significant assets the IRS can reach (OIC becomes nearly impossible)

- The debt is primarily from trust fund taxes (payroll taxes carry personal liability that doesn't disappear in most resolution paths)

Rappaport Tax Relief is direct about this. Not every situation ends in a dramatic settlement. Some cases resolve through structured payment plans. Some through penalty removal. Some through a combination. What matters is getting the right resolution for your actual situation. Not the one that sounds best in a sales pitch.

Waiting feels safe. It's actually the most expensive move you can make.

Frequently Asked Questions

How do I know if I actually qualify for an Offer in Compromise?

The IRS uses a formula called Reasonable Collection Potential to decide whether to accept an OIC. It looks at your income, expenses, and asset equity. If what you can realistically pay over the remaining collection period is less than what you owe, you may qualify. But the calculation is specific and unforgiving. A professional can run the numbers before you submit anything.

What happens if I just ignore IRS notices and don't respond?

The IRS escalates automatically. A CP14 becomes an LT11, which becomes a Notice of Intent to Levy, which becomes an actual levy on your bank account or wages. There's no point in the sequence where ignoring the problem makes it smaller. The collection statute is ten years. The IRS has time, and it uses it.

Can the IRS really garnish my wages without warning?

Not entirely without warning. The IRS is required to send a Final Notice of Intent to Levy before taking wage action. But that notice can arrive and go unnoticed, especially if you've moved or aren't opening mail. By the time you feel the garnishment, the IRS has already completed the required steps. Acting on the first notice is always better than responding to the last one.

Is it too late to get help if a levy has already started?

No. Levies can be released. But it requires immediate action and documentation. The IRS will release a levy if you enter into an approved resolution agreement, demonstrate financial hardship, or show the levy is creating an economic hardship that prevents you from meeting basic living expenses. Rappaport Tax Relief handles IRS levy situations directly and can move quickly when enforcement is already active.

What's the difference between a tax lien and a tax levy?

A lien is a legal claim against your property. It affects your credit and your ability to sell assets, but it doesn't take anything immediately. A levy is the actual seizure: your bank account drained, your wages redirected to the IRS. Liens come first; levies follow if the lien doesn't produce payment. Both are serious, but levies require faster response.

How long does tax resolution actually take?

It depends on the path. A streamlined installment agreement can be established in a few weeks. An Offer in Compromise typically takes six to twelve months from submission to decision. Currently Not Collectible status can be requested relatively quickly once financial documentation is assembled. There are no shortcuts, but there are faster and slower paths depending on your situation.

Do I need a tax attorney, or is an Enrolled Agent enough?

For most IRS collection and resolution cases. Installment agreements, OICs, penalty abatement, levy releases. An Enrolled Agent has full authority to represent you before the IRS. Tax attorneys add value when litigation is involved or when there are complex legal questions about liability. David Rappaport's 30+ years as an Enrolled Agent covers the full range of resolution cases that most individuals and small businesses face.

You've Read This Far. Here's the Next Step

If any section of this article described your situation, you already know what the next move is. Not because it's the comfortable choice. But because you've just seen what happens when people wait.

Rappaport Tax Relief offers a free consultation. Not a sales call. A real conversation about your specific situation, what options are realistically available, and what happens if you do nothing. Call or reach out directly. David Rappaport handles these conversations personally.

About the Author

Rappaport Tax Relief is a tax resolution firm based in Westport, Connecticut, specializing in IRS debt negotiation, penalty abatement, installment agreements, and Offer in Compromise representation. Led by Enrolled Agent David Rappaport with more than 30 years of hands-on experience, they serve individuals, self-employed professionals, and small business owners across Connecticut and New England who are dealing with IRS collection activity and need direct, personal representation. Not a call center.

References

IRS via Experian. Standard deduction amounts for 2025 tax year

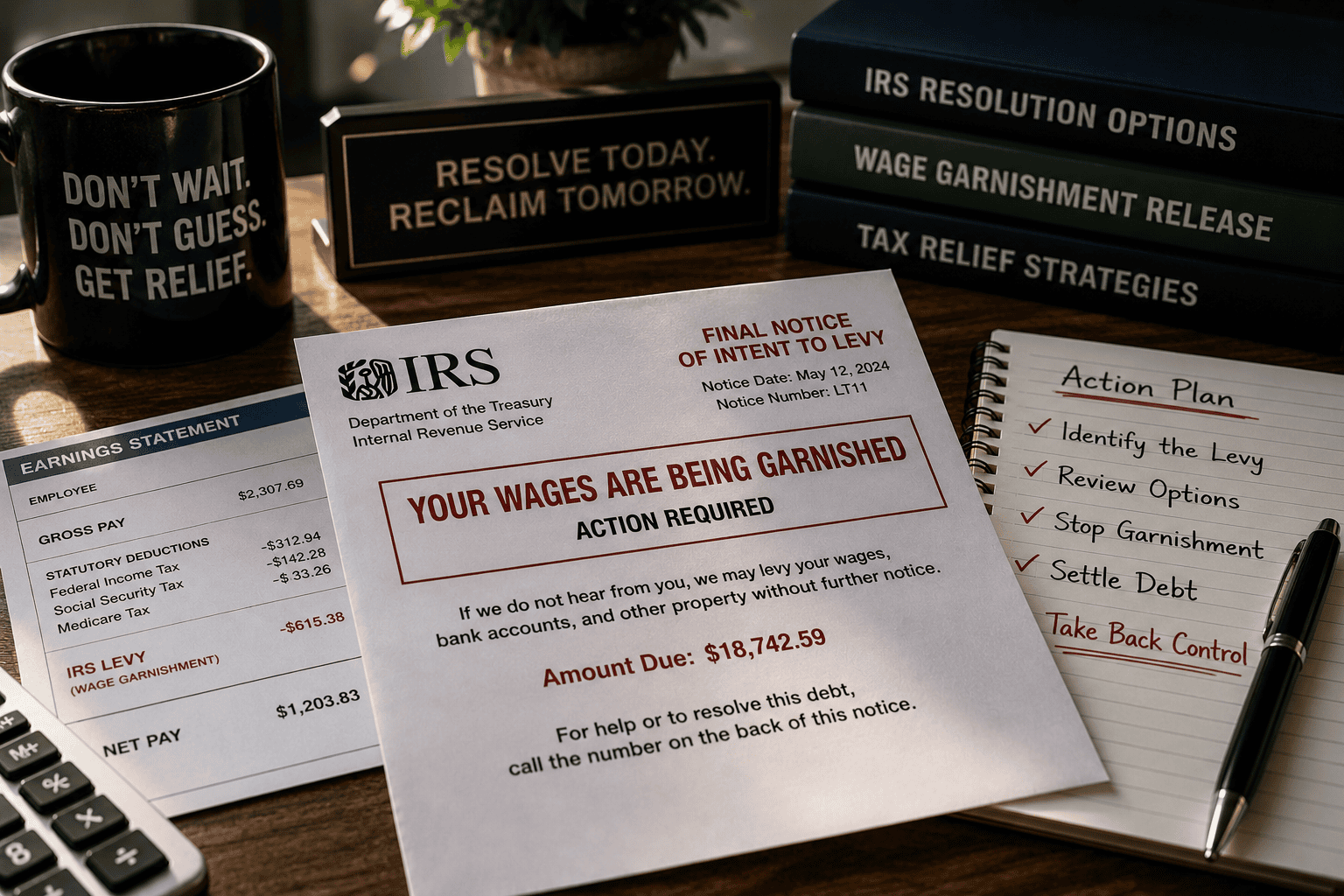

When the IRS Starts Taking Your Paycheck: How Wage Garnishment Release Actually Works

The moment your employer tells you the IRS is taking a cut of your paycheck, something shifts. It's not just the money. It's the exposure, the helplessness, and the creeping fear that this is only the beginning.

A wage garnishment isn't a warning. It's the IRS already inside your finances, and it will keep taking until someone stops it.

Wage garnishment release is the formal process of getting the IRS to stop seizing a portion of your paycheck. It requires either resolving the underlying debt, entering a qualifying payment arrangement, or demonstrating hardship. And it almost always requires direct negotiation with the IRS before your next pay period. Acting fast matters because each pay cycle the garnishment runs costs you money you can't recover.

Key Takeaways

- The IRS can garnish a far larger share of your paycheck than a private creditor. Federal consumer credit protections cap ordinary garnishments at 25% of disposable earnings, but IRS wage levies follow a different, often harsher formula

- Garnishment doesn't stop automatically when you call the IRS. It stops when a specific release condition is met and the IRS formally notifies your employer

- The most common release paths are: installment agreement, currently-not-collectible status, offer in compromise, or demonstrated hardship

- Every pay cycle the garnishment runs is money gone permanently. There's no refund once the IRS collects it

- Rappaport Tax Relief can intervene directly with the IRS on your behalf, often stopping garnishment faster than going it alone

Why Does the IRS Have More Power Over Your Paycheck Than a Regular Creditor?

Most people assume wage garnishment works the same way regardless of who's collecting. It doesn't.

Under the Consumer Credit Protection Act, Title III, private creditors are limited to garnishing 25% of your disposable earnings. Or the amount by which your earnings exceed 30 times the federal minimum wage, whichever is less. That's the legal ceiling for most debt collectors.

The IRS doesn't operate under that ceiling in the same way. Federal tax levies on wages follow IRS Publication 1494, which uses a table based on your filing status and number of dependents to determine the exempt amount. Whatever's left above that exempt threshold is fair game. And for many workers, that means the IRS can take significantly more than 25%.

The practical result: a private creditor garnishment might sting. An IRS wage levy can gut a paycheck.

This is the part most people don't realize until it's already happening to them. The IRS isn't bound by the same rules as a credit card company or a landlord pursuing a judgment. It has statutory collection authority that bypasses the court process entirely. Which is why it can move so fast and why stopping it requires a specific, procedurally correct response.

What Actually Triggers a Wage Garnishment. And What Comes Before It

The IRS doesn't garnish wages without warning. What feels sudden usually isn't.

Before a levy hits your paycheck, the IRS is required to send a series of notices: a balance due notice (CP14), a demand for payment, and a Final Notice of Intent to Levy with your right to a Collection Due Process hearing. That last notice, typically an LT11 or Letter 1058, is the last formal checkpoint before enforcement begins.

Most people who end up garnished either ignored those notices, didn't understand what they meant, or genuinely couldn't pay and didn't know there were options. The IRS doesn't interpret silence as hardship. It interprets silence as an invitation to escalate.

If you've received a CP1058 letter or similar final notice, the window to act before enforcement is narrow. But it exists.

The Four Paths to Wage Garnishment Release

Wage garnishment release is not a single process. It's one of four outcomes, each with different eligibility requirements and timelines.

Installment Agreement. If you can't pay in full but can pay something, the IRS will typically release a levy once an installment agreement is in place. The IRS wants compliance more than it wants to keep garnishing. A structured installment agreement formally resolves the collection action and stops the paycheck seizure.

Currently Not Collectible (CNC) Status. If paying anything right now would leave you unable to cover basic living expenses, the IRS can classify your account as currently not collectible. This pauses collection activity, including the garnishment, while the status holds. It's not forgiveness, but it's breathing room.

Offer in Compromise. An offer in compromise is a negotiated settlement where the IRS agrees to accept less than the full amount owed. While an OIC is pending, collection activity is typically suspended. This is a longer process with strict eligibility requirements, but for the right situation, it can resolve the debt at a fraction of the balance.

Demonstrated Hardship or Error. If the garnishment itself was issued in error, or if it's causing genuine economic hardship beyond normal collection standards, you can request a release on those grounds. This requires documentation and direct engagement with the IRS. It doesn't happen by asking nicely over the phone.

The path that's right for you depends on your income, your total balance, your filing history, and whether you have assets the IRS might pursue separately. Getting this wrong, choosing the wrong resolution path, can close off better options.

The Garnishment Resolution Framework: A Decision Map

The Levy Response Triage framework is a four-question decision tool for identifying the fastest appropriate release path before a single IRS call is made.

Use it when: you've received a wage levy notice or your employer has already been contacted.

- Can you pay the full balance within 120 days? If yes. A short-term payment plan stops the levy fastest.

- Can you pay something, but not the full balance? If yes. An installment agreement is the target. Hardship-based plans exist for low-income filers.

- Would any payment leave you unable to cover rent, food, or utilities? If yes. CNC status is the priority. Document your expenses first.

- Is your total debt significantly less than what you could realistically pay over your remaining earning years? If yes. An offer in compromise may be worth pursuing, but it takes longer and the garnishment may continue during review unless a separate release is negotiated.

Don't use this framework as a substitute for professional review. Use it to walk into that first conversation knowing which direction you're likely heading.

What Happens After the Release Is Granted?

This is the question most people don't think to ask until they're already in the process.

When the IRS grants a levy release, it issues a formal notice to your employer. Your employer then stops the withholding. But not immediately on the day the release is issued. There's typically a processing lag of one to two pay cycles depending on your employer's payroll schedule. You won't get back what was already taken.

The garnishment release also doesn't resolve the underlying debt. Whatever arrangement triggered the release, installment agreement, CNC status, OIC, that's now the active obligation. If you miss a payment or fall out of compliance, the IRS can reinstate the levy without going through the full notice sequence again.

Compliance going forward isn't optional. It's the condition under which the release stays in effect.

This is why working with someone who manages the full picture, not just the immediate crisis, matters. Rappaport Tax Relief approaches this as a lifecycle problem: stopping the garnishment is the first step, but staying out of the IRS's collection queue is the actual goal. You can read more about why hiring a professional for tax debt settlement matters and why the negotiation process is different when someone with standing is making the call.

Going It Alone vs. Getting Represented: The Real Comparison

The most expensive decision in a wage garnishment situation isn't the professional fee. It's the pay cycles lost while you figure out the process yourself.

| Situation | Going It Alone | With Rappaport Tax Relief |

| Speed to release | Slower. Learning the process while it runs | Faster. Direct IRS contact, known procedures |

| Resolution path accuracy | Risk of choosing wrong option, closing off better ones | Assessed against full picture: income, debt, filing history |

| Ongoing compliance | Easy to miss requirements, triggering reinstatement | Managed through the agreement period |

| Future exposure | Debt still exists; collection can resume | Past, present, and future tax issues addressed together |

| Cost of inaction | Every pay cycle costs real money, permanently | Professional fee is a fraction of what continued garnishment takes |

The IRS doesn't give credit for effort. It responds to procedurally correct requests made by people who know the rules.

A Typical Garnishment Scenario

Consider a self-employed contractor in Connecticut who stopped filing for two years during a slow period, then went back to salaried work. The IRS filed substitute returns on his behalf, typically at the least favorable filing status, and assessed a balance higher than his actual liability. By the time he got an LT11 notice, the levy was already in motion.

In a case like this, the right move isn't just stopping the garnishment. It's filing the correct returns to replace the IRS substitutes, which often reduces the actual balance significantly, and then negotiating the resolution from that corrected number. Stopping the levy without fixing the underlying return leaves money on the table. Sometimes thousands of dollars.

The garnishment is the symptom. The unfiled or incorrect returns are the root cause.

Who This Matters Most For

Wage garnishment release is most urgent when you're a salaried employee or W-2 contractor with no other income source. Because the garnishment hits every single pay cycle with no flexibility. It's also critical for small business owners who pay themselves through payroll, since a levy on payroll can effectively shut down operations.

If you have unfiled returns in addition to the garnishment, what self-employed individuals in Connecticut owe the IRS is worth understanding before you make your first call. Because the sequence of steps matters, and getting it out of order can complicate the release.

This process is harder, not impossible, but harder, if you've already defaulted on a previous installment agreement or if there's an active federal tax lien filed against you. Those situations require a more careful approach, but they're not dead ends.

What Rappaport Tax Relief Does Differently

David Rappaport has spent more than 30 years as an Enrolled Agent working directly with the IRS on behalf of individuals and small businesses. Enrolled Agent status means federal authorization to represent taxpayers before the IRS at every level. Audits, appeals, collections.

The concierge approach at Rappaport Tax Relief means you're not handed off to a case manager after the intake call. David works your case personally. That matters in garnishment situations because the IRS responds to representatives who know the file. Not to someone reading from a script.

The goal isn't just the release. It's getting you to a place where the IRS isn't a recurring crisis in your life.

Frequently Asked Questions

How fast can a wage garnishment actually be stopped?

It depends on the resolution path and how quickly documentation is assembled, but once an installment agreement or hardship determination is in place, the IRS is required to release the levy. Your employer then needs a processing cycle to implement it. Realistically, a few weeks from first contact to cleared paycheck is possible. But only if the process moves without delays.

Will my employer know why my wages are being garnished?

Yes. The IRS sends the levy notice directly to your employer's payroll department, and it specifies that it's a federal tax levy. Your employer is legally required to comply and is not permitted to fire you solely because of a single garnishment. But they will know.

Can the IRS garnish my wages if I'm self-employed or a freelancer?

Not through payroll. But the IRS can levy your bank accounts, seize accounts receivable, and intercept payments from clients. The mechanism is different, but the effect is the same. Self-employed individuals face a different collection exposure that requires a different response strategy.

What if I can't afford to pay anything at all right now?

Currently Not Collectible status exists specifically for this situation. If your basic living expenses consume your income, the IRS can suspend collection activity. It doesn't erase the debt, but it stops the garnishment and gives you time to stabilize. You'll need to document your financial situation thoroughly.

Does filing for bankruptcy stop a wage garnishment?

An automatic stay triggered by bankruptcy filing does halt most IRS collection activity temporarily, including wage levies. But bankruptcy has significant long-term consequences and doesn't discharge most federal tax debt. It's a serious option that requires careful analysis. Not a quick fix.

What happens if I ignore the garnishment and just let it run?

The IRS keeps taking until the debt is paid in full, or until you take action. There's no point at which it stops on its own. Every pay cycle that passes is money permanently gone, and the underlying penalties and interest continue to accumulate on any remaining balance.

How is Rappaport Tax Relief different from a national tax relief company?

National firms typically use a volume model. Intake teams, case managers, and limited access to the person actually negotiating. Rappaport Tax Relief is a concierge practice led by David Rappaport personally. You work directly with the Enrolled Agent handling your case, not a support staff layer. For people in Connecticut and the surrounding region, that direct relationship changes the quality of the representation.

The Next Step Isn't Complicated

If your wages are being garnished right now, or if you've received a final notice and haven't responded yet, the most important thing you can do is talk to someone who can assess your actual options. Not a general overview, but your specific situation, your balance, your filing history, your income.

Rappaport Tax Relief offers a free consultation. Not a sales call. A real conversation about where you stand and what the realistic paths forward look like. Call before your next pay cycle runs.

About the Author

Rappaport Tax Relief is a tax resolution practice based in Westport, Connecticut, specializing in IRS debt negotiation, wage garnishment release, and comprehensive tax problem resolution. Led by Enrolled Agent David Rappaport with more than 30 years of hands-on experience, the firm works directly with individuals, self-employed professionals, and small business owners facing IRS collection activity, unfiled returns, and accumulated tax debt. Rappaport Tax Relief serves clients throughout Connecticut and the surrounding region with a concierge approach that addresses past, present, and future tax issues under one roof.

References

U.S. Consumer Credit Protection Act, Title III. Wage garnishment limits for ordinary creditors and support obligations