How Rappaport Tax Relief Actually Works: The End-to-End Process Most Providers Never Explain

The IRS does not get emotional about collections. It just keeps moving — sending notices, escalating to garnishments, freezing accounts — on a schedule that doesn't pause because you're overwhelmed or don't know what to do next. If you've been living with that pressure for months, you already know the worst part isn't the debt itself. It's not knowing how any of this gets resolved.

What Does a Tax Resolution Service Actually Do From Start to Finish?

Tax resolution is a structured negotiation process in which a licensed representative — such as an Enrolled Agent — intervenes between a taxpayer and the IRS to stop active collection, assess the full scope of the tax problem, and negotiate a legal resolution such as an Offer in Compromise, installment agreement, or penalty abatement. The process typically takes three to twelve months depending on complexity, and it addresses past debt, current compliance, and future filing simultaneously.

Key Takeaways

- An Enrolled Agent has federally granted authority to represent you before the IRS at every level — the same authority as a tax attorney, without the legal billing rates.

- The IRS collection process follows a predictable escalation sequence; knowing where you are in that sequence determines which resolution tools apply.

- Filing unfiled returns is almost always the first required step before any negotiation can begin — you cannot negotiate on debt the IRS hasn't fully calculated yet.

- Rappaport Tax Relief handles past, present, and future tax issues under one roof — not just the immediate crisis.

- Most people wait too long to act, which narrows the available resolution options. Earlier intervention consistently produces better outcomes.

Why Does the IRS Keep Escalating Even After You've Tried to Respond?

Here's the part most people don't understand: responding to the IRS on your own — calling the number on the notice, sending a letter, even making a partial payment — does not pause the collection clock unless you've formally established a resolution agreement or filed for representation.

The IRS collection process operates on an automated escalation sequence. A notice goes unresolved, it moves to the next stage. A wage garnishment notice is issued, it becomes active in roughly 30 days. A bank levy can execute the same day it's authorized. The system isn't designed to wait for you to figure things out.

The root cause of most unresolved tax debt isn't financial — it's procedural. People respond informally to a formal process, and the IRS keeps moving because no formal stop has been placed.

This is why representation matters mechanically, not just emotionally. When a licensed Enrolled Agent files a Power of Attorney (Form 2848) with the IRS, all communication must route through them. The IRS cannot contact you directly. That single step changes the dynamic immediately — not because the debt disappears, but because the escalation sequence pauses while a resolution is being formally pursued.

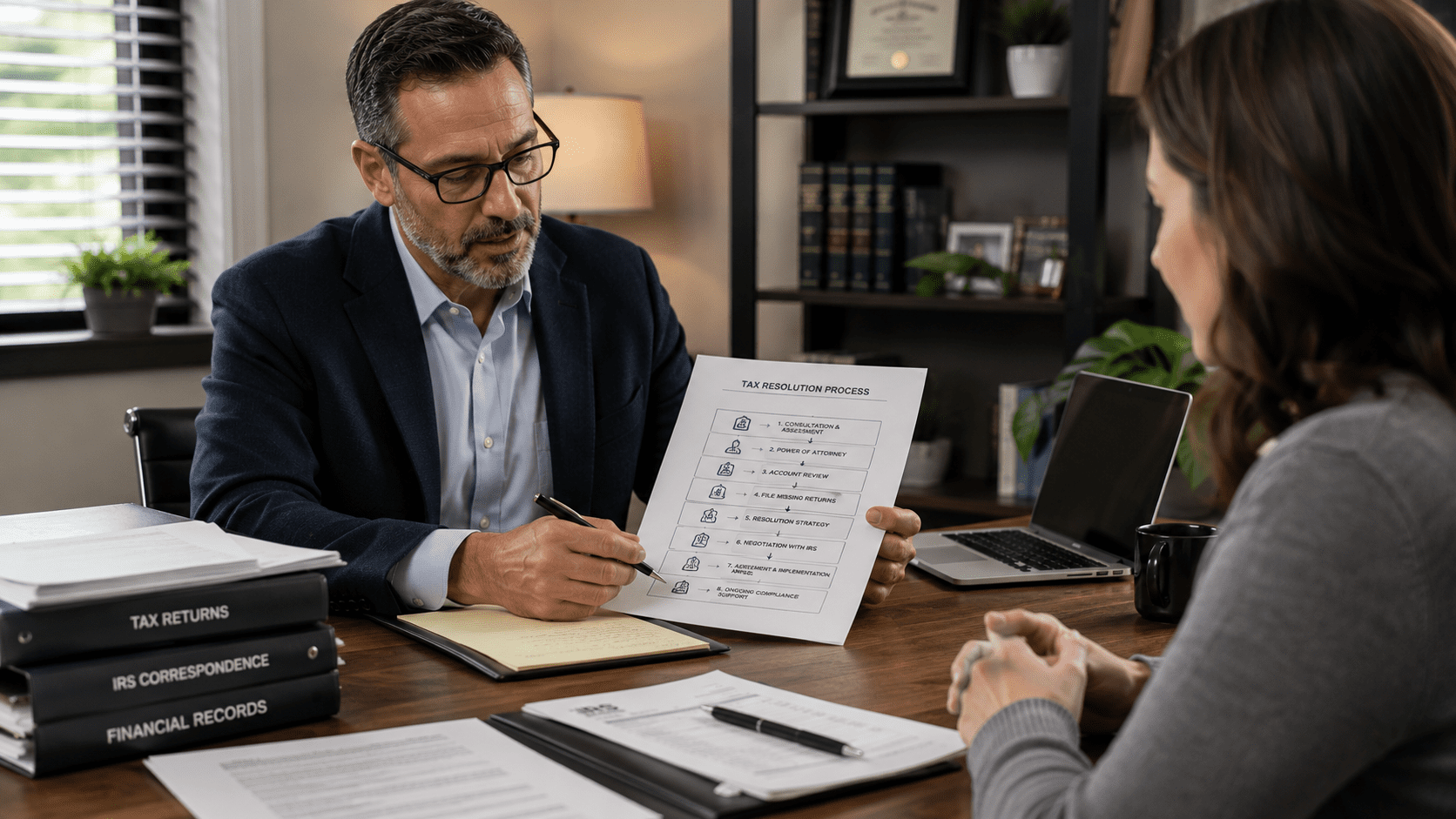

What Actually Happens Step by Step When You Work With Rappaport Tax Relief?

This is the process most providers obscure — either because they want to keep it mysterious or because they're handing your case to a junior staffer you'll never meet. Here's how it actually works, end to end.

Step 1: Free Consultation and Situation Assessment

The process begins with a conversation, not a form. David Rappaport — an Enrolled Agent with 30+ years of hands-on experience — personally reviews your situation. This isn't a screening call. It's a substantive assessment of what you owe, what's been filed, what's been ignored, and where you are in the IRS collection sequence.

Step 2: Filing the Power of Attorney

Once you engage Rappaport Tax Relief, Form 2848 is filed. From this point forward, the IRS communicates with David, not with you. This is the formal stop that most people don't know exists — and it's the mechanism that immediately reduces the daily stress of living under IRS pressure.

Step 3: Transcript Analysis and Full Liability Calculation

Before any negotiation can begin, the full picture has to be established. IRS account transcripts are pulled to determine exactly what's owed, what penalties have accrued, and whether any assessments are incorrect. Tax professionals commonly observe that IRS records contain errors more often than taxpayers expect — and catching those errors early can meaningfully reduce the final liability.

Step 4: Filing Any Missing Returns

Unfiled returns are not optional. The IRS will not negotiate on debt it hasn't finalized, and missing returns are often what's holding up any resolution. Rappaport Tax Relief prepares and files all outstanding returns as part of the process — this is a critical step that some providers treat as a separate, billable add-on.

Step 5: Identifying the Right Resolution Tool

This is where experience matters most. There are multiple IRS resolution programs, and the right one depends on your specific financial situation — not on which program sounds best.

The resolution tool that looks most appealing on a website is rarely the one that applies to your actual situation. Matching the right program to the right taxpayer requires knowing what the IRS will and won't accept — and that knowledge only comes from doing this for decades.

The major options include:

| Resolution Tool | What It Is | Best For | Realistic Outcome |

| Offer in Compromise (OIC) | Settle for less than full amount owed | Taxpayers with limited assets and income | IRS accepts roughly 40% of OIC applications (IRS Data Book) |

| Installment Agreement | Structured monthly payment plan | Those who can pay over time | 3–6 year repayment terms common |

| Currently Not Collectible (CNC) | Temporary halt to collections | Taxpayers with no current ability to pay | Collections paused; reviewed periodically |

| Penalty Abatement | Reduction or removal of penalties | First-time noncompliance or reasonable cause | Can reduce total balance significantly |

| Wage Garnishment Release | Formal IRS release of garnishment | Salaried employees with active garnishments | Often resolved within days of representation |

Step 6: Negotiation and Resolution

With the correct program identified, Rappaport Tax Relief negotiates directly with the IRS. This phase requires documentation, financial disclosures, and often back-and-forth with IRS agents. It is not a one-call process. It is methodical, and it takes time — typically three to twelve months for full resolution depending on complexity.

Step 7: Future Compliance Planning

This is the step almost every other provider skips. Resolving past debt without addressing the conditions that created it means you'll be back in the same situation in three years. Rappaport Tax Relief's concierge accounting model includes ongoing support for current and future tax compliance — quarterly estimated taxes for the self-employed, bookkeeping guidance for small business owners, and annual filing support.

Is an Offer in Compromise Really Achievable, or Is It Just Marketing?

The Offer in Compromise is the most advertised and most misunderstood tax resolution tool in existence. According to the IRS Data Book, the IRS accepts roughly 40% of submitted OIC applications — which means the majority are rejected.

The contrarian truth: an OIC is not the goal. The right resolution is the goal.

Practitioners using a thorough financial analysis approach report that many clients are better served by a well-structured installment agreement or a Currently Not Collectible status than by an OIC that gets rejected and delays resolution by a year. The OIC is powerful when it applies. It doesn't always apply.

A real example of how this plays out: a self-employed contractor three years into penalty accrual, with $47,000 owed and inconsistent income, was assessed as a poor OIC candidate based on IRS reasonable collection potential calculations. Instead, a 60-month installment agreement was negotiated, penalties were partially abated under first-time abatement policy, and the effective amount paid was reduced by roughly 30% from the original balance. Resolution completed in nine months.

The IRS is not your adversary in the way most people imagine. It is a bureaucracy with rules — and rules can be worked with, when you know them.

How Is This Different From Hiring a Tax Attorney or a National Tax Relief Company?

The differences are real, and they matter.

A tax attorney is appropriate when criminal tax charges are involved or when litigation is likely. For the vast majority of IRS debt situations — garnishments, levies, unfiled returns, installment agreements — an Enrolled Agent has identical representation authority at a substantially lower cost.

National tax relief companies operate on volume. Cases are assigned to case managers who rotate, documentation gets lost, and clients frequently report months passing without meaningful updates. The model is built for throughput, not for the kind of situation where someone needs to actually understand what's happening with their case.

Rappaport Tax Relief operates differently by design. David Rappaport personally handles client cases — not a team of coordinators. That's not a marketing claim. It's the structural difference between a concierge practice and a call center with a tax license.

Most tax relief companies sell you a process. Rappaport Tax Relief gives you a practitioner.

Who Is This Not Right For?

Honest answer: not every situation is a fit.

If your tax debt involves criminal tax fraud allegations, you need a tax attorney with criminal defense experience — not a resolution service.

If you owe less than $1,000 and have no enforcement actions pending, a CPA or tax preparer can likely handle it without a full resolution engagement.

If you're unwilling to provide complete financial documentation, no resolution process will work. The IRS requires full financial disclosure for OIC and installment agreement applications. Incomplete disclosures get rejected.

And if you're looking for a quick fix that requires no effort on your part — that doesn't exist. What Rappaport Tax Relief does is carry the burden and handle the complexity. But the process requires your participation.

Frequently Asked Questions

How long does it actually take to resolve IRS tax debt? It depends on which resolution path applies, but most cases take between three and twelve months from engagement to final resolution. Simpler installment agreements can be established faster. An Offer in Compromise typically takes six to twelve months because the IRS has its own review timeline. The process doesn't move faster by pushing harder — it moves faster by submitting complete, accurate documentation the first time.

Will the IRS really stop contacting me once I hire someone? Yes — once a Power of Attorney (Form 2848) is filed with the IRS, all IRS communication must go through your representative, not to you directly. This is a legal requirement, not a courtesy. It's one of the most immediate practical benefits of professional representation.

Can I really settle my tax debt for less than I owe? Sometimes, yes — through an Offer in Compromise. But the IRS approves roughly 40% of OIC applications, and eligibility depends on your income, assets, and expenses relative to what the IRS calculates as your reasonable collection potential. A practitioner who tells you an OIC is guaranteed before reviewing your financials is not being straight with you.

What happens if I have years of unfiled tax returns? Unfiled returns have to be filed before most resolution options become available. The IRS will not negotiate a settlement on debt it hasn't fully assessed. Rappaport Tax Relief prepares and files outstanding returns as part of the resolution process — it's not a separate problem, it's the starting point.

I'm self-employed and my income varies a lot — does that hurt my case? Variable income actually works in your favor in some resolution scenarios, particularly for Offer in Compromise eligibility calculations. The IRS uses an average of recent income to assess your ability to pay. A practitioner who understands how to document irregular income correctly can present your financial picture more accurately than a generic form submission.

What's the difference between an Enrolled Agent and a tax attorney for IRS issues? An Enrolled Agent is a federally licensed tax professional with full authority to represent taxpayers before the IRS — the same representation rights as a tax attorney. The practical difference is cost and specialization: Enrolled Agents focus specifically on tax matters and typically charge less than attorneys. For the vast majority of IRS debt situations, an Enrolled Agent is the appropriate choice.

What if I've already tried to resolve this on my own and made it worse? It's more common than you'd think. Partial payments, informal agreements, or missed deadlines can complicate a case — but they rarely make it unresolvable. The first step is a full transcript analysis to understand exactly where things stand. Rappaport Tax Relief has worked with clients who came in after years of trying to handle it themselves, and the situation was still fixable.

You Don't Have to Keep Running From This

If you've read this far, you already know more about how tax resolution actually works than most people who've been living with IRS debt for years. That knowledge matters. But knowing the process and having someone execute it for you are two different things.

The weight of an unresolved tax problem doesn't get lighter by waiting. It compounds — in penalties, in enforcement actions, in the daily low-grade dread of not knowing what comes next.

Rappaport Tax Relief offers a free consultation with David Rappaport directly. Not a form. Not a callback from a case coordinator. A real conversation about your specific situation, what options exist, and what the path forward looks like.

If you're ready to stop managing the anxiety and start resolving the problem, that conversation is the next step.

Schedule your free consultation at rappaporttaxrelief.com.

References

IRS Data Book — Annual publication covering IRS enforcement statistics, Offer in Compromise acceptance rates, and collection activity data. Published by the Internal Revenue Service.

IRS.gov — Official source for IRS collection procedures, Form 2848 (Power of Attorney), and taxpayer resolution program eligibility requirements.

How to Tell If a Tax Relief Company Is Actually Going to Help You (Or Just Take Your Money)

The IRS does not get emotional about collections. It just keeps moving — letters, levies, garnishments, one after another — until someone stops it. And when you're already overwhelmed, the pressure to hire someone fast makes you exactly the kind of person predatory tax relief companies are built to exploit.

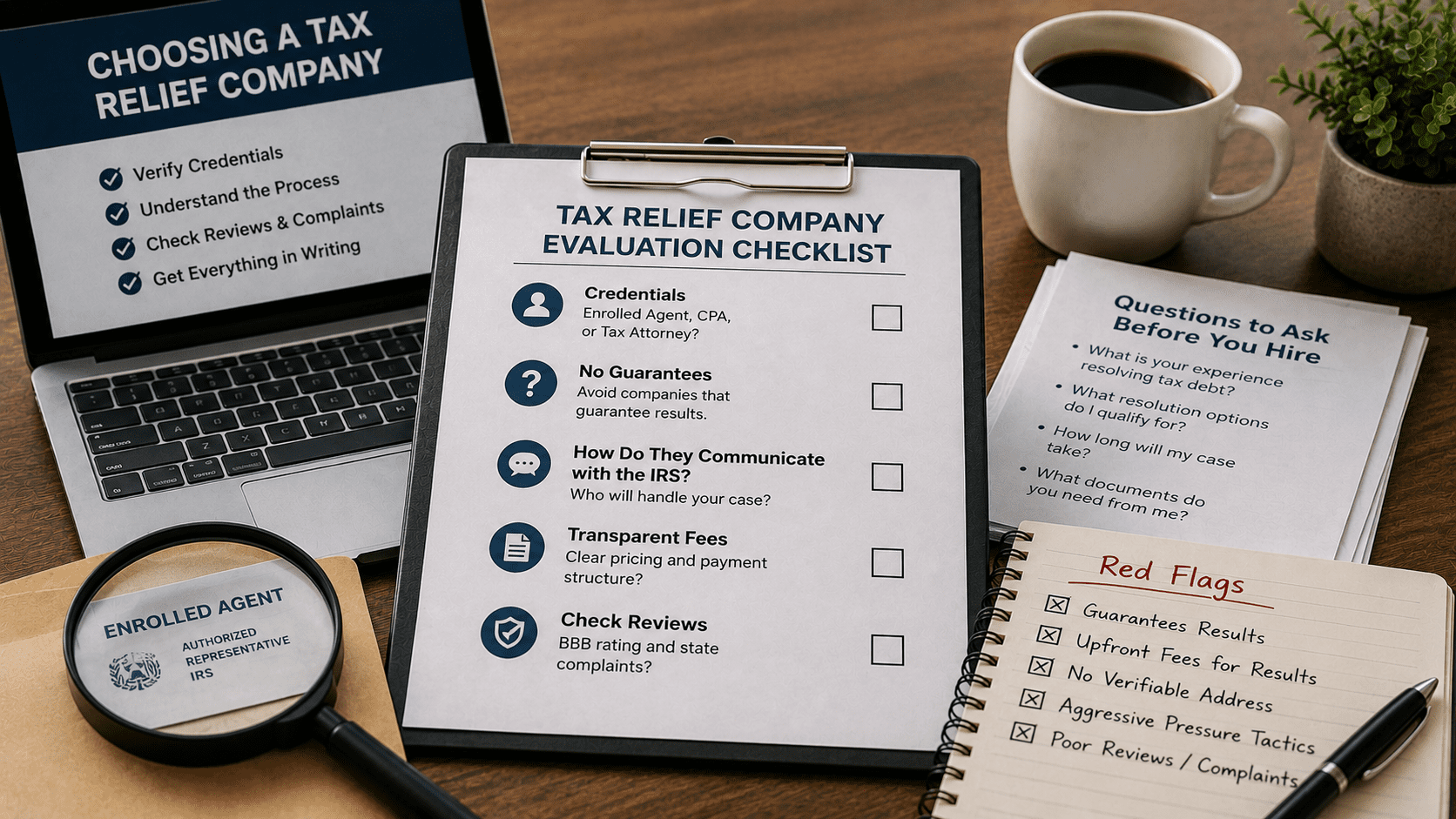

Directly answering the question: To evaluate a tax relief provider without being misled, verify the representative's credentials (Enrolled Agent, CPA, or tax attorney), confirm they offer a free consultation before charging fees, ask specifically how they communicate with the IRS on your behalf, and check their complaint history with the Better Business Bureau and your state attorney general. Avoid any firm that guarantees a specific outcome before reviewing your case.

Key Takeaways

- Legitimate tax relief providers hold verifiable credentials — Enrolled Agent (EA), CPA, or licensed tax attorney. Ask for the credential number and check it.

- No ethical firm guarantees a specific resolution amount before reviewing your full financial picture.

- The IRS Restructuring and Reform Act of 1998 established taxpayer rights that your representative should be actively using on your behalf — if they can't name them, that's a problem.

- Resolution timelines are real: most Installment Agreements take 30–90 days to finalize; Offers in Compromise average 6–12 months per IRS processing guidelines.

- A provider who handles past, present, and future tax issues under one relationship costs less in aggregate than cycling through separate specialists.

Why Do So Many People Hire the Wrong Tax Relief Company?

The tax relief industry is largely unregulated at the marketing level. Anyone can run ads promising to "settle your tax debt for pennies on the dollar." The credential barrier to advertising tax relief is zero. The barrier to actually practicing before the IRS is significant — but most people don't know the difference until they've already paid a retainer.

This is the root cause: the gap between what a company promises in an ad and what they're legally authorized to do is invisible to someone who has never navigated IRS collections before. Predatory firms exploit that information asymmetry deliberately.

The mechanism works like this: fear compresses decision-making. When a wage garnishment hits your paycheck or a levy freezes your bank account, the psychological pressure to act immediately overrides the instinct to research carefully. Firms that advertise aggressively know this. They time their outreach — and their urgency language — to catch people at exactly that moment.

The single most expensive mistake in tax resolution isn't hiring the wrong firm — it's hiring the wrong firm fast, because panic replaced judgment.

What Credentials Actually Mean — and Which Ones Matter

Enrolled Agent (EA) is the only credential issued directly by the IRS — it grants unlimited practice rights before the IRS at all levels, including audits, collections, and appeals. CPAs and tax attorneys also hold full practice rights. Anyone else — a "tax consultant," "tax specialist," or unlicensed preparer — cannot represent you before the IRS in any meaningful capacity.

This distinction is not semantic. If your representative cannot appear before the IRS on your behalf, you are still effectively unrepresented. You're paying for paperwork help, not advocacy.

The IRS maintains a public directory at irs.gov/tax-professionals where you can verify any EA's credentials by name. Use it. A legitimate firm will tell you to check.

David Rappaport of Rappaport Tax Relief holds Enrolled Agent status with over 30 years of hands-on IRS negotiation experience — the kind of practitioner-level depth that comes from working actual cases, not just knowing the code.

The Practitioner's Evaluation Framework: The CLEAR Test

The CLEAR Test is a five-point evaluation framework for assessing any tax relief provider before signing anything or paying a retainer.

Use this when you're comparing providers or feeling pressured to decide quickly. Skip it only if you've already verified credentials independently and have a referral from someone whose situation matched yours.

| Criterion | What to Ask | Red Flag |

| C — Credentials | "What is your EA or CPA license number?" | Vague titles, no verifiable number |

| L — Limitations Disclosed | "What outcomes can you NOT guarantee?" | Any firm that won't name limitations |

| E — Explicit Process | "Walk me through exactly what happens after I hire you." | Generic answers, no IRS-specific steps |

| A — Access to Principal | "Who personally handles my case?" | "A team" with no named practitioner |

| R — Resolution Range | "What's a realistic range of outcomes for my situation?" | Specific dollar promises before case review |

A firm that passes all five without hesitation is worth a serious conversation. A firm that stumbles on two or more is telling you something important.

What Does "Concierge" Tax Resolution Actually Mean in Practice?

Most national tax relief firms operate on volume. Your case is assigned to a case manager — not a credentialed practitioner — who follows a script and escalates when things get complicated. You may never speak to the person who actually knows tax law.

Concierge tax resolution is the opposite model: one credentialed practitioner manages your case from intake through resolution, knows your file, and is reachable when something changes.

Why this matters mechanically: IRS collection cases are not static. A revenue officer can escalate, a levy can be issued between scheduled calls, a Collection Due Process hearing deadline can pass. When your case is handled by someone who knows it deeply, those developments get caught and responded to. When it's handled by a rotating case manager working from notes, they don't.

Rappaport Tax Relief operates on this model specifically. David Rappaport personally handles client cases — not a junior associate, not a call center. That's not a marketing line. It's a structural difference in how the work gets done.

Knowing your case file is not a luxury in tax resolution — it's the difference between catching a deadline and missing it permanently.

What Realistic Outcomes Actually Look Like (With Numbers)

Here's what practitioners commonly observe across resolution types — not guarantees, but honest ranges based on IRS program parameters.

Installment Agreement: A self-employed contractor with $34,000 in back taxes and no prior defaults can typically establish a streamlined installment agreement within 30–60 days. Monthly payments are based on ability to pay, not the full balance divided arbitrarily.

Offer in Compromise (OIC): The IRS accepted roughly 13,000–15,000 OICs annually in recent reporting years (IRS Data Book). Acceptance is based on Reasonable Collection Potential — a specific IRS formula weighing assets, income, and allowable expenses. A business owner three years into penalty accrual, with $67,000 in assessed liability but documented income below IRS Collection Financial Standards, resolved to $11,200 over 11 months through an accepted OIC. That outcome required a complete financial disclosure, accurate documentation, and a practitioner who knew how to present the case — not just file the form.

Currently Not Collectible (CNC) Status: For clients with income at or near IRS allowable expense thresholds, CNC status pauses collection activity entirely. It doesn't eliminate the debt, but it stops the bleeding while circumstances change.

Rappaport Tax Relief works across all three resolution tracks — and the right path depends entirely on your specific financial picture, not on which program sounds most appealing.

Who This Approach Is NOT Right For

Honest assessment matters here.

Tax resolution services are not the right fit if your total IRS liability is under $5,000 and you have the income to pay it — in that case, a direct IRS payment plan costs nothing to set up and requires no representation.

If your situation involves criminal tax fraud allegations, you need a tax attorney with criminal defense experience, not an Enrolled Agent. EA authority covers civil IRS matters; criminal exposure is a different legal domain entirely.

And if you're looking for someone to make the problem disappear without your participation — providing financial documents, disclosing income accurately, responding to information requests — no legitimate firm can help you. Resolution requires cooperation. Any firm that promises otherwise is not being straight with you.

Frequently Asked Questions

How do I know if a tax relief company is legitimate before I pay them anything? Ask for the practitioner's Enrolled Agent, CPA, or bar license number and verify it independently through the IRS directory or your state licensing board. Legitimate firms welcome this. Also check the Better Business Bureau and your state attorney general's complaint database — volume complaints about upfront fees with no follow-through are a consistent pattern with bad actors.

What's the difference between an Enrolled Agent and a tax attorney for IRS problems? Both hold unlimited practice rights before the IRS, meaning either can represent you in audits, collections, and appeals. Tax attorneys are better suited when there's potential criminal exposure or complex litigation. Enrolled Agents typically specialize more deeply in IRS procedure and resolution programs — for most collection cases, an experienced EA is exactly the right credential.

Can a tax relief company actually get my wage garnishment stopped quickly? Yes, but "quickly" depends on your situation. Once a practitioner files a power of attorney and contacts the IRS, a garnishment release can sometimes be negotiated within days if you qualify for a resolution program. The IRS does not release garnishments as a courtesy — there needs to be an active resolution in place or a pending appeal. Rappaport Tax Relief handles garnishment releases directly as part of the resolution process.

What happens if I've had unfiled tax returns for several years? Unfiled returns don't disappear — the IRS can file a Substitute for Return (SFR) on your behalf, which almost always results in a higher liability than if you'd filed yourself. Getting into compliance by filing past returns is usually the first step in any resolution process. Practitioners commonly observe that clients who file voluntarily receive more favorable treatment than those whose returns were filed by the IRS.

Is an Offer in Compromise realistic for someone with a modest income? It can be. The OIC program is specifically designed for taxpayers whose Reasonable Collection Potential — what the IRS calculates they can actually collect — is less than the full liability. Modest income can actually support an OIC application if allowable expenses are documented correctly. The form is not the hard part; the financial presentation is.

How long does it take to resolve IRS tax debt completely? It depends on the resolution path. Installment Agreements: 30–90 days to establish. Offers in Compromise: 6–12 months for IRS processing after submission. Currently Not Collectible status: can be established relatively quickly but requires annual review. Complex cases with multiple years of unfiled returns can take longer — but every month without representation is a month of continued penalty and interest accrual.

What should I bring to a free consultation with a tax relief firm? Bring any IRS notices you've received (the notice number in the top right corner tells a practitioner exactly what stage of collection you're in), your most recent tax returns if you have them, and a general sense of your monthly income and expenses. You don't need everything organized — a good practitioner will tell you exactly what they need after hearing your situation.

The One Thing That Changes How You See This Entire Category

Most people treat tax relief as a transaction: pay someone to negotiate a number down. That framing leads to hiring whoever quotes the lowest fee or promises the biggest reduction.

The more accurate frame: tax resolution is access management. The IRS has a defined set of programs, each with specific eligibility criteria and procedural requirements. A skilled practitioner's job is to get you into the right program, present your case correctly, and keep the process moving. The outcome is a function of your financial reality and the quality of the presentation — not the boldness of the promise.

That's what 30 years of hands-on IRS negotiation actually buys you. Not magic. Precision.

If you're at the point where you've read this far, you're not looking for a quick fix. You're looking for someone who will actually handle this — past baggage, present crisis, and a path forward that doesn't leave you back here in three years.

That's exactly what Rappaport Tax Relief does. Schedule your free consultation and talk directly with David Rappaport about where you stand and what's actually possible for your situation.

References

IRS.gov — IRS Data Book (annual publication covering OIC acceptance rates, collection statistics, and taxpayer compliance data)

IRS.gov — Taxpayer Rights under the IRS Restructuring and Reform Act of 1998

IRS.gov — Offer in Compromise program eligibility and Reasonable Collection Potential calculation methodology

IRS.gov — Tax Professional Directory (credential verification for Enrolled Agents)

Better Business Bureau (bbb.org) — Consumer complaint database for tax relief companies

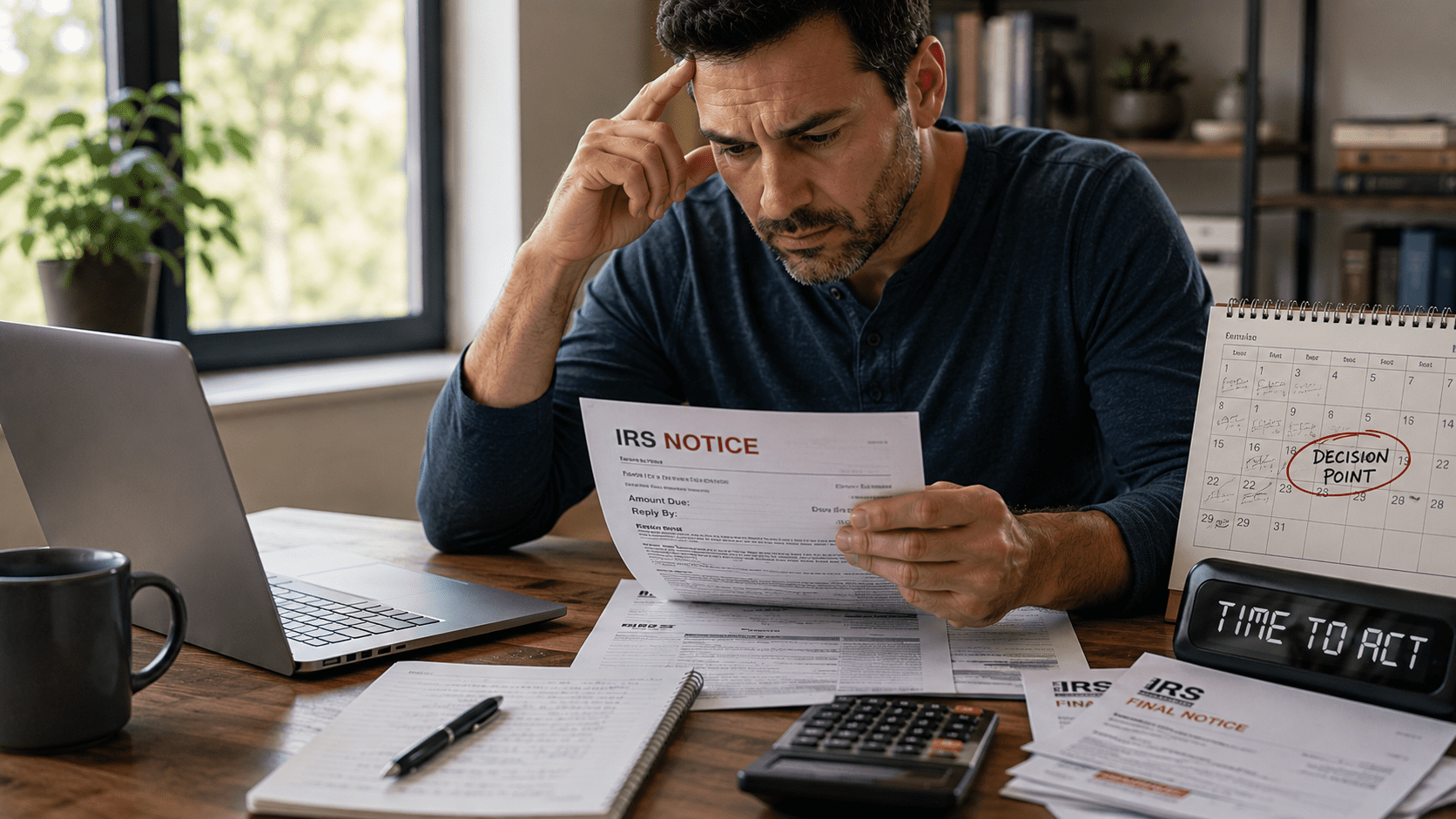

When to Act and When to Wait on Tax Relief: The Timing Signals That Actually Matter

The IRS does not get emotional about collections. It just keeps moving — issuing notices, escalating enforcement, and accruing penalties whether you open the mail or not. If you have tax debt right now, the question is not whether to deal with it. The question is whether the moment you're in calls for immediate action or strategic patience.

Direct Answer

Acting immediately on IRS debt is not always the right move — but waiting without a strategy is almost always the wrong one. The optimal timing depends on where you are in the IRS collection sequence, what resolution options you currently qualify for, and whether your financial picture is stable enough to support a binding agreement. A qualified tax professional can assess these signals and tell you exactly where you stand.

Key Takeaways

- The IRS collection process follows a predictable sequence — knowing where you are in it determines your best move.

- Some resolution options, like an Offer in Compromise, require specific financial conditions to be met before filing; acting too early can result in rejection.

- Wage garnishments and bank levies require immediate action — these are not situations where waiting has any strategic value.

- Unfiled returns create a separate, compounding problem that blocks most relief options until they're resolved.

- A free consultation with an enrolled agent can map your exact position in the IRS timeline and identify which window is open right now.

Why Does Timing Feel So Confusing When You Have Tax Debt?

Most people with IRS debt are not avoiding it because they don't care. They're avoiding it because the situation feels permanently urgent — and when everything feels like a crisis, nothing feels actionable.

That paralysis has a specific cause: the IRS sends notices that all look alarming, but they represent very different stages of the collection process. A CP14 notice (your first balance-due notice) and a CP504 notice (a final notice before levy) are not the same situation. Treating them identically — either by panicking at both or ignoring both — is where most people lose ground.

The IRS collection sequence is a defined bureaucratic process, not a random escalation. Understanding where you are in it is the first act of reclaiming control.

Timing in tax relief is not about moving fast or moving slow — it's about knowing which stage you're in and what that stage allows.

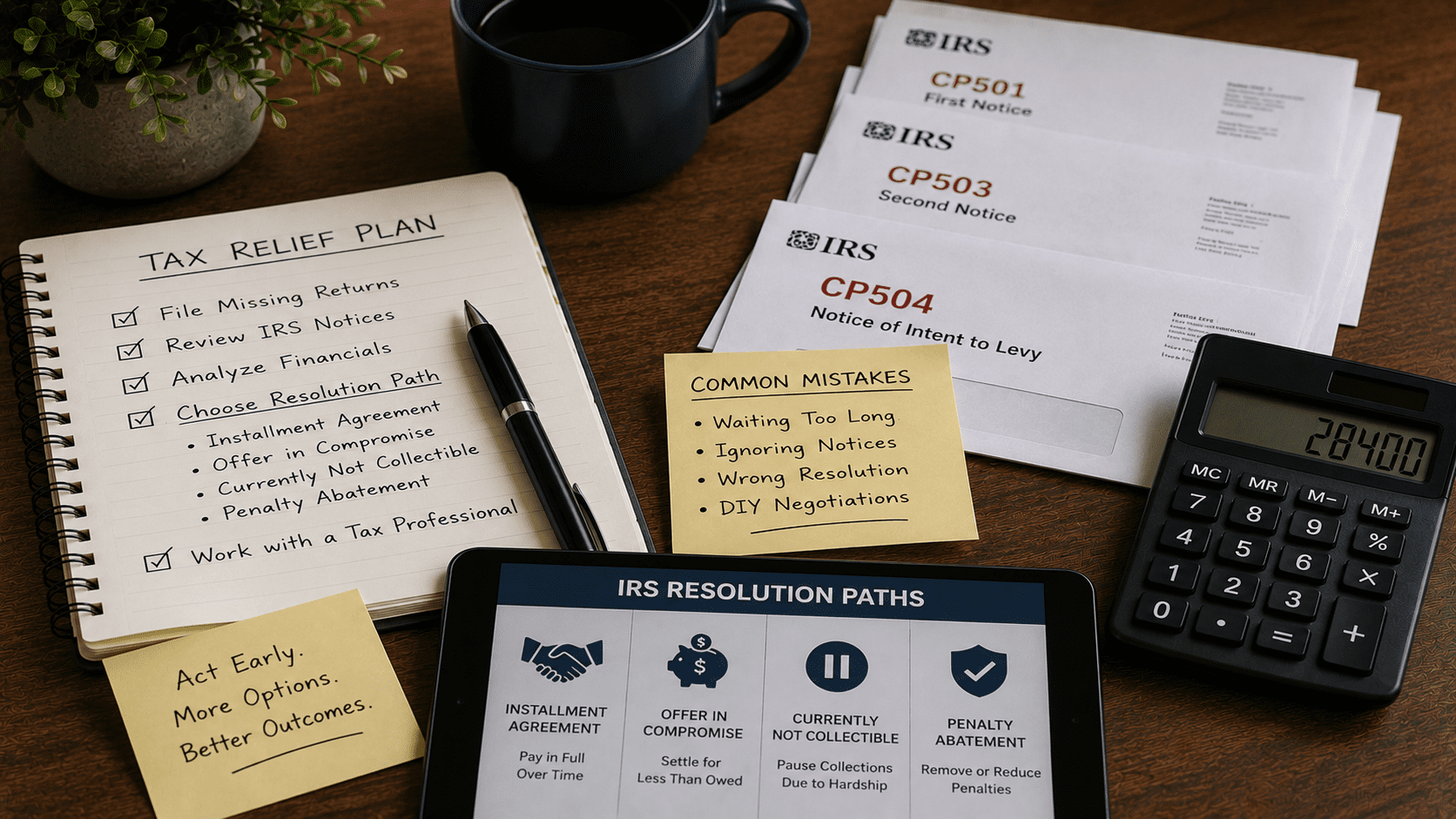

What Is the IRS Collection Timeline and Why Does It Change Your Options?

The IRS collection timeline is the sequential series of enforcement stages the IRS moves through after a tax balance goes unpaid, each with different available responses and narrowing resolution windows.

Here's a simplified map:

| Stage | IRS Action | Your Window |

| CP14 / CP501 | Balance due notice | Wide open — all options available |

| CP503 / CP504 | Escalating notices, intent to levy | Still negotiable, but urgency is real |

| Letter 1058 / LT11 | Final Notice of Intent to Levy | 30-day window to request a Collection Due Process hearing |

| Active Levy / Garnishment | Bank account seized or wages withheld | Immediate intervention required |

| Tax Lien Filed (NFTL) | Public record, credit impact | Resolution still possible; lien withdrawal negotiable |

Most people first call a tax professional somewhere between CP504 and an active levy. That's not ideal — but it's workable. What's not workable is calling after a levy has been running for months and assets have been depleted.

The 30-day window after a Final Notice of Intent to Levy is one of the most consequential deadlines in tax resolution. Missing it doesn't eliminate your options, but it removes your right to a Collection Due Process hearing — a formal appeal mechanism that can pause IRS enforcement while you negotiate.

When Should You Wait Before Filing for Relief?

Here's the contrarian claim: filing for an Offer in Compromise too early can actively hurt you.

An Offer in Compromise (OIC) is a settlement agreement in which the IRS accepts less than the full amount owed, based on the taxpayer's demonstrated inability to pay the full balance. The IRS calculates your "reasonable collection potential" — a formula based on income, assets, and allowable expenses — and compares it to your offer amount.

If your income is temporarily elevated (a strong freelance quarter, a one-time bonus, a seasonal spike), your reasonable collection potential looks higher than your true long-term picture. Filing an OIC in that window typically results in rejection. The IRS will use your current numbers, not your average.

Waiting three to six months until your income stabilizes can be the difference between a rejected offer and an accepted one. This is not procrastination — it's positioning.

The same logic applies to business owners whose revenue is declining. Filing before the decline is documented gives the IRS a rosier picture of your ability to pay.

Tax professionals who understand IRS financial analysis — not just the paperwork — know when to hold the filing and why. This is the kind of judgment that comes from 30+ years of practitioner experience, which is exactly what Rappaport Tax Relief brings to every case.

When Is Waiting Genuinely Dangerous?

Wage garnishment and bank levies are not situations that improve with time.

A wage garnishment is a mandatory withholding from your paycheck, typically leaving you with only a small exempt amount based on IRS tables. A bank levy freezes your account and seizes funds — often before you even know it's happening.

Both require immediate professional intervention. Here's why the mechanism matters: the IRS will not release a garnishment or levy out of goodwill. Release requires either full payment, an accepted installment agreement, a demonstrated hardship, or proof that the levy is creating an economic hardship that prevents basic living expenses. None of those outcomes happen on their own.

A self-employed contractor in New York had wages levied after ignoring notices for 14 months. Within six weeks of engaging Rappaport Tax Relief, the levy was released and an installment agreement was in place. The delay cost him roughly $9,000 in seized income that could not be recovered. The resolution itself cost a fraction of that.

Unfiled returns are a separate emergency. The IRS can file a Substitute for Return (SFR) on your behalf — using only the income information it has, with no deductions, no credits, and no context. The resulting balance is almost always higher than what you would actually owe if you filed correctly. And until those returns are filed, you cannot access most resolution programs at all.

Unfiled returns don't just create debt — they lock you out of every tool that could reduce it.

How Do You Know Which Resolution Path Is Right for Your Situation?

The right resolution path depends on three variables: what you owe, what you earn, and what you own.

The Rappaport Resolution Readiness Framework is a practical three-axis assessment for determining which IRS resolution option is viable right now:

Axis 1 — Liability Clarity: Are all returns filed? If not, resolution options are blocked until filing is current. Start here.

Axis 2 — Financial Stability: Is your income consistent and documented? Stable income supports an installment agreement. Declining or irregular income may support an OIC — but only once the pattern is documented.

Axis 3 — Asset Exposure: Do you have significant equity in property, retirement accounts, or business assets? High asset exposure reduces OIC eligibility but may support a partial payment installment agreement or currently-not-collectible status.

Use this framework when: you're trying to decide whether to act now or wait for a better financial window.

Not when: you have an active levy or garnishment — that situation bypasses the framework entirely and requires immediate intervention.

Rappaport Tax Relief walks every client through this assessment in the initial consultation, at no cost, because the right starting point depends entirely on where you actually are — not where a generic checklist assumes you are.

What Are the Real Tradeoffs Between Acting Now Versus Waiting?

| Scenario | Acting Now | Waiting |

| Active garnishment or levy | Stops the bleeding immediately | Every week costs real money |

| OIC with temporarily high income | Likely rejection, wasted filing fees | Better positioning in 3–6 months |

| Unfiled returns | Opens all resolution options | Blocks every path; IRS may file SFR |

| Early-stage notices (CP14) | Establishes goodwill, more options | Low risk if monitored closely |

| Penalty accrual on large balance | Each month adds 0.5% monthly failure-to-pay penalty (IRS.gov) | Compounding cost with no benefit |

The IRS charges a failure-to-pay penalty of 0.5% of the unpaid balance per month, up to a maximum of 25% of the original balance, per IRS.gov. On a $40,000 balance, that's $200 per month in penalties alone — before interest. Waiting without a strategy is not neutral. It has a measurable cost.

Who Is This Approach Not Right For?

This framework assumes you are dealing with legitimate tax debt and want a legal resolution. It is not a fit for:

- Situations involving suspected tax fraud or criminal investigation — those require a tax attorney, not an enrolled agent.

- Taxpayers who owe less than $1,000 — the IRS has simplified processes for small balances that don't require professional representation.

- Individuals who are already in an active, performing installment agreement with no enforcement actions — if it's working, don't disrupt it.

Rappaport Tax Relief will tell you honestly in the first conversation if your situation falls outside what they can help with. That kind of directness is rare in this industry — and it's the reason clients trust the process.

Frequently Asked Questions

How do I know if the IRS is about to garnish my wages? The IRS is required to send a Final Notice of Intent to Levy (Letter 1058 or LT11) before initiating a wage garnishment. If you've received this letter, you have 30 days to request a Collection Due Process hearing, which pauses enforcement. If you're unsure which notice you have, bring it to a tax professional immediately — the letter type determines your options.

Can I negotiate with the IRS on my own without hiring anyone? Technically yes, but the IRS negotiates using specific financial formulas and procedural rules that most people aren't familiar with. A common mistake is agreeing to a monthly installment amount you can't sustain — which defaults the agreement and restarts enforcement. An enrolled agent knows what the IRS will accept and how to structure an agreement that actually holds.

What happens if I just ignore the IRS notices? The IRS will escalate. Ignoring notices does not pause the process — it accelerates it. The IRS will eventually file a tax lien (which damages your credit and encumbers your property), levy your bank accounts, or garnish your wages. None of these outcomes are reversible without intervention.

Is an Offer in Compromise realistic for most people? The IRS accepts roughly 30–40% of OIC applications in recent years, per IRS Data Book figures. Acceptance depends heavily on whether the offer is properly prepared and timed. Many rejections happen because the offer was filed when the taxpayer's financial picture didn't support it — not because the taxpayer was ineligible in principle.

How long does it take to resolve IRS debt? It depends on the resolution path. An installment agreement can be established in weeks. An Offer in Compromise typically takes 6 to 18 months from submission to resolution. A business owner three years into penalty accrual on a $60,000 balance resolved through an OIC in 11 months with professional representation — the key was waiting until revenue had declined enough to document genuine hardship.

Will getting help with my taxes affect my credit score? The IRS filing a Notice of Federal Tax Lien (NFTL) can affect your credit, since it becomes a public record. Resolving the debt — through an OIC, full payment, or installment agreement — can make you eligible to request lien withdrawal, which removes the public record. Your tax professional can request this as part of the resolution.

What does a free consultation with Rappaport Tax Relief actually cover? The consultation is a real assessment — not a sales call. David Rappaport reviews your notices, identifies where you are in the IRS collection timeline, and tells you which resolution options are currently available to you. You leave with a clear picture of your situation and a recommended next step, whether or not you engage further.

You Don't Have to Figure Out the Timing Alone

If you've read this far, you're not someone who wants to ignore the problem. You want to handle it right.

The hardest part of tax debt isn't the money. It's not knowing whether the moment you're in calls for urgency or patience — and not having anyone in your corner who can tell you honestly.

That's exactly what Rappaport Tax Relief does. David Rappaport has spent 30+ years reading IRS notices, negotiating collection cases, and telling clients the truth about where they stand. The free consultation isn't a pitch. It's a map.

Call Rappaport Tax Relief today and find out exactly where you are in the IRS timeline — and what your best move is right now. Not next month. Now.

Visit rappaporttaxrelief.com to schedule your free consultation.

References

IRS.gov — IRS collection notice sequence, levy procedures, failure-to-pay penalty rates, and Offer in Compromise program guidelines.

IRS Data Book — Annual publication covering IRS enforcement statistics, Offer in Compromise acceptance rates, and collection activity data.

The Most Common Tax Relief Mistakes People Make — And Why They Keep Making Them

The IRS does not get emotional about collections. It just keeps moving — adding penalties, compounding interest, escalating to levies and garnishments — while most people are still deciding whether to open the envelope. That gap between the IRS's momentum and a taxpayer's paralysis is where most tax situations go from bad to genuinely damaging.

Direct Answer

The most common tax relief mistakes people make are waiting too long to act, attempting to negotiate with the IRS without representation, ignoring notices until enforcement begins, and choosing resolution paths that don't match their actual financial situation. These mistakes persist not from carelessness but because the IRS system is designed around compliance, not guidance — leaving taxpayers to navigate it alone.

Key Takeaways

- Ignoring IRS notices doesn't pause the process — it accelerates enforcement timelines and reduces your negotiating options

- Filing late returns, even without payment, stops the penalty clock and reopens resolution pathways that disappear without filed returns

- An Offer in Compromise is not available to everyone — qualifying requires specific financial conditions, and applying incorrectly wastes time and fees

- Installment agreements negotiated without professional help often set monthly payments higher than necessary, creating a new financial crisis

- Enrolled Agents have federally recognized authority to represent taxpayers before the IRS — a distinction that matters when negotiating collection holds

Why Do People Wait So Long to Deal with IRS Debt?

Avoidance is not laziness. It is a predictable response to a system that feels punishing to engage with.

When people receive IRS notices, the instinct is to set them aside until they feel "ready" — financially, emotionally, or practically. The problem is that the IRS operates on fixed statutory timelines. The Collection Statute Expiration Date (CSED) — the 10-year window the IRS has to collect assessed tax debt — does not pause because a taxpayer is overwhelmed. More critically, certain resolution options narrow or close entirely as enforcement escalates.

Waiting does not preserve your options. It eliminates them.

Consider a business owner three years into penalty accrual on a significant payroll tax debt. The balance had grown substantially before they sought help — not because they ignored it intentionally, but because they kept expecting cash flow to recover enough to simply pay it. When they finally engaged Rappaport Tax Relief, the resolution pathway was still available, but the negotiating position had weakened considerably. Had they acted earlier, the balance and the timeline both would have been smaller.

The mechanism here matters: penalties under IRS Code Section 6651 compound monthly. Every month of inaction is not neutral — it is actively expensive. Understanding when to act and when to wait on tax relief can mean the difference between a manageable resolution and a far more costly one.

Is Trying to Handle IRS Debt Yourself Actually a Bad Idea?

Yes. Not because taxpayers are incapable, but because the IRS negotiation process rewards procedural knowledge that takes years to develop.

The IRS's Automated Collection System (ACS) is staffed by agents working from scripts and authority limits. A taxpayer calling in without representation is negotiating blind — they don't know what the agent can actually approve, what financial information to disclose or withhold, or which collection alternative fits their situation. Practitioners report that self-represented taxpayers routinely agree to installment payment amounts that exceed what a professional would have negotiated, because they don't know that Collection Financial Standards — the IRS's own benchmark for allowable living expenses — can be used to lower the required monthly payment.

> The IRS is not your adversary, but it is not your advisor either. It will accept whatever you agree to, even if a better option existed.

This is worth sitting with: the IRS does not tell you about resolution options you don't ask for. Offer in Compromise, Currently Not Collectible status, Penalty Abatement — these are not offered proactively. They require a taxpayer or their representative to initiate and document the request correctly.

Rappaport Tax Relief handles this negotiation on behalf of clients, using more than 30 years of direct IRS experience to identify which pathway fits the actual financial picture — not the one that sounds best in a brochure.

What Is the "Wrong Resolution" Mistake and Why Does It Cost So Much?

Choosing the wrong resolution path is the most expensive mistake most people have never heard of.

The three primary IRS resolution options — Installment Agreement, Offer in Compromise (OIC), and Currently Not Collectible (CNC) status — each have distinct eligibility criteria, cost structures, and long-term implications.

The Resolution Fit Framework is a simple diagnostic tool for understanding which path applies:

| Resolution Path | Use When | Not When |

| Installment Agreement | You can pay the full balance over time | Monthly payment would create financial hardship |

| Offer in Compromise | Your Reasonable Collection Potential (RCP) is less than what you owe | You have assets or income that disqualify you |

| Currently Not Collectible | You have no disposable income after IRS-allowed expenses | You have irregular income that could qualify you for OIC |

| Penalty Abatement | You have a clean compliance history and a reasonable cause | You have prior penalty abatement in the last 3 years |

Use this framework as a starting diagnostic — not a final determination. Eligibility has layers.

The OIC mistake is particularly common. National tax relief advertising has made "settle your debt for pennies on the dollar" a cultural shorthand — but the IRS accepts only a fraction of OIC applications, and applying without meeting the financial threshold wastes months and fees while enforcement continues.

> Choosing the wrong IRS resolution path doesn't just fail — it delays the right path and gives the IRS more time to collect.

Why Do Unfiled Returns Create More Damage Than Unpaid Taxes?

This is the observation that surprises most people: owing money to the IRS is a problem; not filing is a crisis.

Unfiled returns trigger the IRS's Substitute for Return (SFR) process — the IRS files a return on your behalf using only the income information it has, with no deductions, no credits, and no context. The resulting tax assessment is almost always inflated, and it starts the penalty and interest clock immediately.

More critically, an SFR assessment locks you out of certain resolution options until the correct return is filed. You cannot negotiate an Offer in Compromise on an SFR balance. You cannot establish a formal installment agreement in good standing. The IRS requires full compliance — all returns filed — before most resolution pathways open.

Filing, even without the ability to pay, is always the right first move. It stops the SFR process, establishes the accurate balance, and reopens negotiating options. This feels counterintuitive: filing a return that shows you owe money feels like making the problem worse. It actually makes it solvable.

Rappaport Tax Relief regularly helps clients file multiple years of back returns as the first step in a resolution plan — because without that foundation, nothing else can move forward.

Does Hiring a National Tax Relief Company Actually Help?

Sometimes. But the tradeoffs are real and worth understanding.

National tax relief firms operate at volume. They use intake teams, case managers, and rotating representatives — meaning the person who assessed your situation is rarely the person negotiating with the IRS on your behalf. Clients of large national firms often wait months before substantive IRS contact is made, while penalties continue to accrue. Knowing how to tell if a tax relief company is actually going to help you before signing anything can save significant time and money.

The structural difference with a concierge approach — like the one Rappaport Tax Relief provides — is continuity. David Rappaport, an Enrolled Agent with more than 30 years of IRS negotiation experience, handles client cases personally from the firm's Westport, Connecticut office. The person who knows your financial situation is the person speaking to the IRS. That continuity is not a comfort feature. It is a negotiating advantage, because the IRS responds to representatives who can answer questions in real time without putting the call on hold to check a file.

| Factor | National Firm | Concierge EA (Rappaport) |

| Case handler continuity | Often rotates | Single practitioner |

| IRS contact timeline | Can be delayed | Initiated promptly |

| Personalization | Standardized intake | Individual financial analysis |

| Geographic familiarity | Generic | Connecticut and surrounding area context |

| Fee structure | Often upfront, large retainer | Transparent, case-specific |

The One Insight Worth Bookmarking

The IRS's collection system is not designed to find the resolution that helps you most — it is designed to collect as much as possible, as quickly as possible. Getting the outcome you deserve requires someone who knows how to ask for it.

Who Is Tax Relief Representation NOT Right For?

Honest answer: not everyone needs full representation.

If you have a single year of unfiled returns, a straightforward income history, and the ability to pay the balance in full within 120 days, a self-service IRS payment arrangement may be sufficient. The IRS's Online Payment Agreement tool handles simple cases without professional involvement.

Rappaport Tax Relief is built for situations with more complexity: multiple years of debt, active enforcement like wage garnishments or bank levies, business payroll tax issues, or cases where the balance has grown significantly through penalties. If your situation is simple and contained, say so during a free consultation — an honest practitioner will tell you when you don't need them.

What this service does not do: it does not provide criminal defense for tax fraud or evasion. Those situations require a tax attorney with criminal law experience. Enrolled Agent authority covers civil IRS matters — audits, collections, appeals, and resolution — not criminal proceedings. For those who want to understand how Rappaport Tax Relief actually works from end to end, that process is laid out in detail for prospective clients before any engagement begins.

Frequently Asked Questions

How long does it actually take to resolve IRS debt? Resolution timelines vary by case complexity, but most straightforward installment agreements are established within 60 to 90 days of engagement. Offer in Compromise cases typically take 6 to 12 months from submission to IRS decision, sometimes longer if the IRS requests additional documentation. Cases involving unfiled returns add time at the front end, because returns must be filed before resolution negotiations can formally begin.

Will the IRS really negotiate with me, or is that just marketing? The IRS does negotiate — but only within specific programs it administers, and only when the taxpayer or their representative initiates the request with proper documentation. The IRS does not proactively offer you the best available option. It accepts what you agree to. Having a representative who knows what to ask for, and how to document it, is what makes negotiation meaningful rather than performative.

What happens if I just ignore IRS notices and hope they go away? They don't go away. The IRS follows a structured notice sequence — CP14, CP501, CP503, CP504, and then enforcement action — and each stage escalates collection authority. Ignoring notices does not pause this sequence; it advances it. Once the IRS issues a Final Notice of Intent to Levy, they can garnish wages, seize bank accounts, or place liens on property. Acting before that final notice is issued preserves significantly more options.

Can I get my wage garnishment stopped quickly? Yes, in most cases a wage garnishment can be released relatively quickly once a resolution pathway is established. The IRS will typically release a levy when a taxpayer enters into an installment agreement or demonstrates financial hardship. The process requires direct IRS contact, proper documentation, and in some cases same-day or next-day action. Rappaport Tax Relief has helped clients stop garnishments before the next payroll cycle.

Is an Offer in Compromise actually realistic for someone with a modest income? It can be, and modest income is actually one factor that can support OIC eligibility. The IRS calculates your Reasonable Collection Potential (RCP) — essentially what they believe they can actually collect from you — and if that number is less than the total balance owed, an OIC may be viable. The mistake is assuming you qualify without a proper financial analysis, or assuming you don't qualify without one. A professional assessment is the only way to know.

What's the difference between an Enrolled Agent and a CPA or tax attorney for IRS issues? An Enrolled Agent (EA) is a federally licensed tax practitioner with unlimited rights to represent taxpayers before the IRS — including audits, collections, and appeals. CPAs and attorneys can also represent taxpayers, but their core training is in accounting and law respectively. EAs specialize specifically in taxation and IRS procedure. For IRS collection and resolution work, an experienced EA often has more direct, specialized IRS negotiation experience than a general CPA or attorney.

What should I bring to a first consultation with a tax relief professional? Bring any IRS notices you've received, your most recent tax returns (or note how many years are unfiled), a general sense of your income and major assets, and any correspondence about garnishments or levies. You don't need everything organized perfectly — the consultation is designed to assess your situation, not audit you. The goal of the first conversation is to understand what you're dealing with and identify the fastest path to stopping enforcement.

You Don't Have to Keep Carrying This

If you've read this far, you're not someone who doesn't care about resolving this. You're someone who hasn't known where to start — or who started in the wrong place and got burned.

Rappaport Tax Relief offers free consultations because the first step shouldn't cost you anything. Call or reach out at rappaporttaxrelief.com, tell David what you're dealing with, and get a straight answer about what your options actually are. Not a sales pitch. Not a generic plan. A real conversation about your specific situation — from someone who has resolved cases like yours for more than 30 years, right here in Westport, Connecticut.

The IRS keeps moving whether you're ready or not. Now is a better time than next month.

References

IRS.gov — IRS collection notice sequence, levy and garnishment procedures, Offer in Compromise eligibility guidelines, and Collection Financial Standards

IRS.gov — Substitute for Return (SFR) process documentation and taxpayer compliance requirements

IRS.gov — Enrolled Agent licensing authority and scope of representation before the IRS (Circular 230)

IRS.gov — Collection Statute Expiration Date (CSED) rules and IRS Code Section 6651 penalty provisions